The market is mostly analyzing two stories in isolation. One is the AI infrastructure boom: chips, power, campuses, GPU clouds, AI factories, and multi hundred billion-dollar capex plans. The other is the quiet stress beginning to show up in private credit: gated vehicles, semi-liquid funds meting hard redemption limits, widening skepticism around marks, and a general reminder that illiquid assets cannot offer liquid experiences forever.

Source: Bloomberg, TheDailyEconomy

The more interesting question is what happens if those two stories are not separate. What happens if private credit is not merely adjacent to the AI boom, but part of the financial plumbing enabling it?

That is the core thesis. The risk is not that AI infrastructure is imaginary. The risk is that some meaningful share of the buildout may be funded through structures that suppress visible volatility, defer price discovery, and assume capital remains patient. If that assumption breaks, the pressure may not show up first where the underlying assets sit. It may show up where liquidty lives.

The hidden transmission channel

The intuitive mistake investors make is to think that if an asset class is illiquid, it is insulated. In practice, illiquidity can do the opposite. It can trap stress until investors need cash, at which point they do not sell the assets they would most like to exit. They sell what they can. In this cycle, what they can sell is often the large, liquid public winners that dominate portfolios and indices.

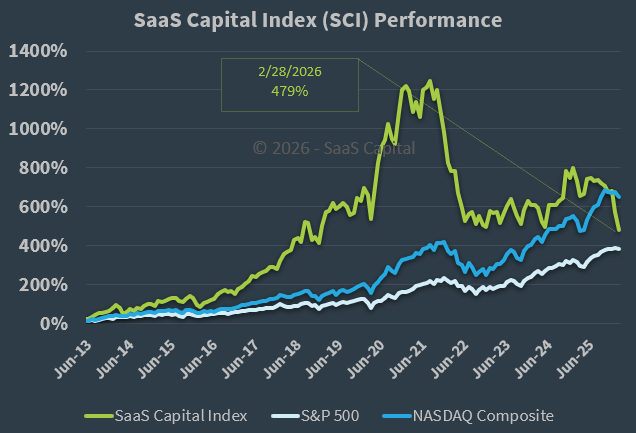

Source: SaaS Capital

That is how private market fragility can become public-market volatility without any dramatic deterioration in the underlying public companies themselves.

The chain is simple enough to sound almost obvious once stated. AI infrastructure gets funded privately. Private marks remain smooth because the assets are long-dated, negotiated, and not continuously marked to an open market. Stress emerges somewhere in the system, whether through slower than expected utilization, higher refinancing costs, power delays, construction overruns, customer concentration, or just a broader liquidity event. Investors in semi-liquid or illiquid vehicles want money back. Managers cannot or will not sell the underlying loans quickly at clean prices. So they gate, stretch distributions, defend marks, or extend maturities. Investors needing liquidity then go elsewhere. They sell public AI winners, liquid semis, Mag 7 exposure, data center proxies, or anything else large and monetizable. In that scenario, public tech becomes the ATM for pressure hiding in private structures.

That is the note.

The ingredient is the liquidity and duration mismatch

The elegance of the idea is that it does not require fraud, nor does it require the AI boom to be fake. It only requires a mismatch between the duration and liquidity of the assets being financed and the expectations of the capital supporting them. We have seen versions of that movie many times. The details change; the structure does not.

What makes the current moment interesting is that AI infrastructure is unusually well-suited to this kind of funding tension. These are capital-intensive assets. They often involve long timelines, bespoke contracts, staggered deployment, specialized equipment, heavy construction, power and interconnection work, and uncertain residual values across rapidly evolving hardware generations. That naturally pushes financing toward private channels: private credit funds, direct lending, structured facilities, vendor financing, warehouse lines, project-level debt, private converts, asset-backed structures, and bespoke capital stacks that sit outside public scrutiny. None of that is inherently bad. In fact, it may be necessary. But it does mean that a large and highly visible boom may be resting partly on a much less visible financing layer.

That matters because private credit does not eliminate volatility. It changes where volatility lives. In public markets, volatility is visible immediately because prices move every day. In private markets, volatility often appears first as narrative control. Marks stay smooth. Funds describe issues as timing, not impairment. Managers talk about long-duration value creation. Drawdowns become negotiations rather than price prints. That can be fine for a while. It becomes dangerous when investors mistake the absence of daily marks for the absence of real risk.

This is where AI enthusiasm may be unintentionally helping the system look cleaner than it is. A powerful secular narrative can make almost any financing structure look more sensible than it otherwise would. If demand is presumed to be exploding, if hyperscaler capex is assumed to be durable, if GPU scarcity is assumed to support high pricing, then long-dated capital structures feel justified. Private lenders can underwrite against growth. Managers can hold marks firm. Investors can accept illiquidity because they believe they are financing something structurally necessary. In that environment, the AI boom and private-credit smoothness reinforce each other. One supplies the story. The other supplies the capital.

The problem emerges when financing assumptions begin to matter more than the story itself. That is the point where investors discover that “AI demand is real” and “this capital structure is resilient” are not the same claim. A project can make sense over ten years and still produce acute financial stress over eighteen months if funding, utilization, and liquidity do not line up cleanly.

This is why I do not think the right analogy is 2008 in the sensational sense. It is probably not a classic bank-plumbing crisis unless leverage is more deeply embedded in systemically important balance sheets than currently assumed. The more plausible analogy is slower and more modern: delayed price discovery, gated liquidity, stretched capital structures, refinancing stress, and cross-asset selling pressure as investors raise cash from the liquid sleeve of their portfolios. In other words, not necessarily a solvency crisis first, but a transmission crisis first.

That distinction matters. In a classical crisis, the asset at the center collapses and takes the system with it. In a transmission event, the asset at the center may remain economically valuable, but the financing around it becomes the amplifier. That is what makes this theme interesting. AI infrastructure may turn out to be a perfectly good long run asset class. That does not mean the path through which it got financed is robust.

There is also an important psychological dimension. Public investors tend to grant a premium to visible winners in a powerful secular theme. They want to own the obvious beneficiaries: semis, hyperscalers, liquid infrastructure names, and whatever publicly traded proxies best map onto the boom. Private investors, by contrast, often get sold the calmer version of the same boom: contracted cash flows, floating-rate loans, low-volatility marks, steady distributions, and the message that they are earning attrctive yield on mission-critical infrastructure. That sounds diversified. In practice, it can be a hidden concentration. Both pools of capital are effectively riding the same macro narrative, just in different wrappers.

That is where the transmission channel becomes potent. If the private wrapper starts to crack, the public wrapper may be the easiest thing to sell.

Where the investment work lives

The next question is what would actually trigger the chain. It does not need to be an AI crash. It could be something more ordinary and therefore more dangerous. A rise in funding costs. Delayed power energization. A slower-than-expected customer ramp. Lwer pricing on leased compute as supply broadens. Residual value questions on hardware generations that age faster than underwritten. A broader market shock that forces allocators to raise liquidity wherever they can. The trigger matters less than the structure. Once investors in semi-liquid vehicles need cash and cannot get it cleanly from the underlying portfolio, the hunt for liquidity moves elsewhere.

This is why the theme is important for public-equity investors even if they never touch private credit. Public holders of AI winners may believe they are underwriting earnings, margins, supply chains, and capex cycles. They may in fact also be underwriting their role as a liquidity reservoir for privatemarket stress. That is not a reason to avoid the names. It is a reason to interpret volatility differently. A sharp selloff in a public AI leader may not always be a signal about deteriorating fundamentals. It may sometimes be a signal about pressure elsewhere in the capital stack.

That possibility creates a strange but valuable implication. If the thesis is right, then public AI volatility could occasionally overshoot fundamentals because it is serving two functions at once: price discovery for its own business and liquidity source for stresses outside itself. That can be painful in the short run but potentially attractive for patient capital that can distinguish between transmission selling and true impairment.

The deeper bearish version of the note is not that AI capex will collapse. It is that the market may learn that some portion of what it took to be secular AI conviction was actually confidence in the financing stack behind the buildout. Those are not the same thing. When the financing stack is easy, secular stories feel cleaner. When it tightens, the story does not necessarily die, but it becomes more expensive, more selective, and more unevenly distributed across participants.

That is why this note matters now. Most investors are still separating the AI capex story from the private credit stress story. But the most interesting risks in markets usually come from exactly these hiden junctions, where one narrative is funding another without the market fully acknowledging the connection.

The strongest version of the thesis is not dramatic. It is simply this: AI infrastructure may be one of the most important economic buildouts of the next decade, and private credit may be one of the least appreciated financial mechanisms helping it happen. If that is true, then the next air pocket in public AI equities may not begin in semiconductors, software demand, or hyperscaler guidance. It may begin in private market vehicles that cannot turn long-duration optimism into short-duration liquidity.

Leave a comment