Intro

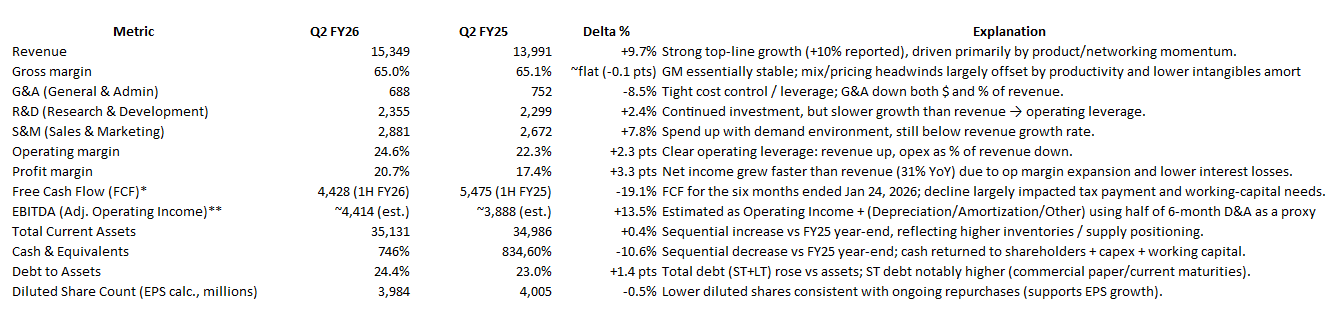

Cisco’s most recent quarter reads like more than a routine beat-and-raise cycle. Revenue grew roughly 10% year over year to $15.35B, but the more telling feature was the shape of the growth: product strength drove the upside, and networking was the engine room. At the same time, profitability expanded, operating income rose to $3.78B from $3.11B a year ago, translating into a higher operating mrgin.

What makes this setup interesting is that Cisco is trying to do something markets rarely allow in one package: keep behaving like a recurring revenue compounder while also capturing a hardware led AI buildout. Subscription revenue in the quarter was $7.836B, which is about half of total revenue, reinforcing that the model still has a meaningful “annuity-like” base underneath the current cycle.

Against that fundamental backdrop, the chart looks like “Wyckoff “markup to high-level range.” That’s often what it looks like when institutions have already repriced the stock once and are now deciding whether the next leg is a continuation (re-accumulation) or the beginning of a topping process (distribution).

The investment thesis

The way to frame Cisco today is that it’s being repriced from “mature networking plus dividend” into something closer to “critical AI-era infrastructure with platform optionality.” The market is not debating whether Cisco is executing, this quarter suggests it is. The debate is whether the new growth is structural (repeatable, multiyear, worthy of multiple expansion) or cyclical (pulled forward demand, lumpy hyperscaler spend, followed by normalization).

This matters because the stock’s next move likely won’t be decided by a single datapoint like “AI orders.” It will be decided by whether Cisco can demonstrate that new demand converts into durable revenue streams while keeping the model intact: gross margins, cash conversion, and the recurring base.

Fundamentals: what’s actually changing

Networking is back as the driver, not an afterthought

In Q2 FY26, Cisco reported $15.349B in total revenue versus $13.991B in the prior-year quarter, and product revenue rose materially. The key detail is the mix: networking revenue was $8.294B, up from $6.850B, about 21% growth and this makes all the difference to market participants. This is not a subtle shift. For years, investors treated Cisco networking as slow, replacement driven, and vulnerable to budget cycles. This print is the opposite: networking is behaving like a segment with real momentum.

Cisco’s own framing is consistent with the AI and campus narrative: product growth was driven by AI infrastructure and campus networking solutions, while security softness reflected product transitions and the Splunk shift toward cloud subscriptions.

Operating leverage is doing more work than buybacks

The quarter’s quality shows up in the income statement. Operating income increased to $3.781B from $3.113B and operating margin expanded to roughly 24.6% from 22.3%. Net income rose to $3.175B from $2.428B, lifting net margin to about 20.7%.

What’s notable is how “clean” that leverage is. R&D was up only modestly year over year, sales and marketing rose but not faster than revenue, and G&A actually declined. This is precisely the mix of growth and discipline that markets reward when their considering a multiple re-rate.

Cisco is more recurring than most people admit, even during a hardware wave

The recurring base is not an abstract talking point in this filing. Cisco reported $7.836B of subscription revenue for the quarter (product subscription plus services subscription). Against total revenue of $15.349B, that’s roughly half the business.

This matters because it reframes what “hardware acceleration” means. If Cisco were purely a “boxes and maintenance” company, an AI/networking hardware wave would create big upside followed by a painful hangover. But a substantial subscription base changes the slope of the downside: the stock can still de-rate, but the business is less likely to collapse.

The supply chain commitment is the quiet signal that Cisco believes the cycle is real

One of the most underappreciated tells in the 10-Q is balance sheet behavior. Inventories increased to $3.920B from $3.164B at FY25 year-end, and inventory purchase commitments rose to $10.062B from $7.604B. The filing attributes the increase to higher commitments tied to Cisco Silicon One and other products and the need to secure components, including memory.

This is meaningful because it is management putting working capital at risk to meet demand. That can be prescient (you win share and deliver growth) or dangerous (you build inventory into a slowdown). In Wyckoff terms, it’s the kind of behavior that typically precedes either a sustained continuation, or a painful “distribution revealed” moment if demand doesnt follow.

Visibility isn’t exploding, but it isn’t deteriorating either

RPO at quarter end was $43.406B, with product RPO up modestly and long-term product RPO also higher. This isn’t the kind of number that screams “hypergrowth,” but it does support the idea that Cisco isn’t simply pulling forward revenue at the expense of the out-period.

The market’s pushback: why Cisco isn’t already priced like a full AI winner

The reason Cisco isn’t universally treated as the next AI infrastructure compounder”

” is that the market can see the friction points.

Gross margin, for example, is not collapsing in the reported quarter, consolidated gross margin is essentially flat year over year, but investors are focused on what happens next as hardware mix increases and memory/component costs flow through. A company can post strong growth and still fail to re-rate if investors conclude the margin structure will deteriorate.

Security is another optical headwind. Security product revenue declined in the quarter, and Cisco explains that the decline is being driven by prior-generation product pressure as well as Splunk consumption shifting toward cloud subscriptions, which creates near-term revenue drag. The platform story may be right, but markets want the reported numbers to stop looking messy.

Finally, cash flow timing can matter more than investors expect in a hardware ramp moment. The combination of higher inventory, higher purchase commitments, and component dynamics can pressure near term cash conversion even if the long-term demand picture is attractive. This is where sentiment can flip quickly if the tape senses the business is over-committing.

The technicals lens: what price action is saying about the fundamentals

This chart reads like a classic two-act sequence. First, the stock went through a sustained markup through 2024 and 2025, punctuated by a sharp selloff that looks more like a shakeout than a trend change given the subsequent recovery. Second, price put in a strong surge into early 2026 and then settled into a high-level range.

Wyckoff calls this kind of range “cause.” The market is effectively building the setup for the next meaningful move, but it hasnt declared direction. That direction tends to be determined by whether fundamentals confirm the new narrative.

If this is re-accumulation, you typically see support hold repeatedly, downswings lose urgency (supply dries up), and rallies begin to show ease of movement. In fundamentals language, that would correspond to clean AI order-to-revenue conversion, campus refresh durability, and stabilization of margin concerns.

If this is distribution, you tend to see repeated failures near the highs, deterioration in structure, and eventually a break of the range floor followed by weak retests. Fundamentally, that’s the world where hyperscaler demand proves too lumpy, margin pressure persists, and security/observability remains optically weak for longer than the market’s patience.

How to underwrite Cisco: a barbell stock with an “offensive” upside and a “defensive” base

Cisco increasingly trades like a barbell. On the defensive side, it has meaningful deferred/contracted work and a business model that is roughly half subscription, plus ongoing capital return capacity. Cisco has also maintained meaningful repurchase authorization, with roughly $10.7B remaining under the program as of quarter end.

On the offensive side, it has AI data center networking and optics momentum and a campus refresh cycle that can broaden demand beyond hyperscalers. The barbell is why the stock can consolidate at highs: some investors are underwriting it as an AI-era winner; others are treating it as a mature company enjoying a late-cycle boost.

Risks / thesis breakers

The clearest Wyckoff-style risk is a clean break of the range floor followed by a failure to reclaim it, because that would imply institutions are using strength to distribute. Fundamentally, the risk catalysts are margin deterioration that proves more structural than transitory, hyperscaler lumpiness that makes growth hard to forecast, and a security segment that remains stuck in transition optics.

Bottom line

I view Cisco as constructively bullish in this setup, but not in the “set it and forget it” way. This is a “prove it” tape. The business is showing credible fundamental momentum, networking is strong, operating leverage is real, and the recurring base remains meaningful.

The chart, read through suggests the market is building cause after a markup. If Cisco validates durability, through conversion, margins, and cleaner platform optics, this range can resolve as re-accumulation and set up the next advance. If it doesn’t, the same range may later be recognized as distribution. Right now, the tape is saying: the first repricing happened; the second one has to be earned.

Disclaimer: This text expresses the views of the author as of the date indicated and such views are subject to change without notice. The author has no duty or obligation to update the information contained herein. Further, wherever there is the potential for profit there is also the possibility of loss. Additionally, the present article is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Some information and data contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. The author trusts that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.

Leave a comment