Nvidia’s results are out and the company is trading like the equity wrapper on a new industrial buildout: power-constrained, token-producing AI factories. The stock is consolidating because investors aren’t debating whether demand is big; theire debating how durable the spend is, how smooth the Blackwell to Rubin transition will be, and how much of the economics NVIDIA can keep.

Quick notes:

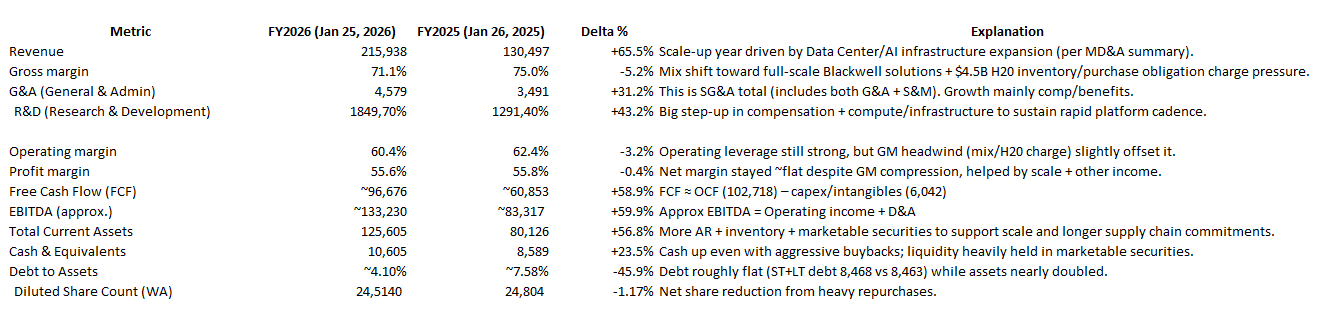

This is the “AI factory prime contractor” model showing up in the financials:

Share count drifting down tells you management is actively converting this cycle into per-share compounding (even before you argue about multiple expansion).

Revenue +65% with opex up far less (+41%) is the core bull signal: scale its outrunning the cost base, even with NVIDIA reinvesting aggressively in R&D.

Gross margin compression (75% to 71.1%) is exactly what you’d expect during a platform/mix transition into more complete systems, and it’s also explicitly tied to the $4.5B H20 charge. The question for the stock is whether GM re-expands as the new platform matures or stays structurally lower because “full-stack” is heavier.

FCF is still exploding (+59%) even though working capital is clearly scaling (inventories and receivables ramping with the business). That’s the “demand is real + supply is tight” signature: you’re funding the ramp and still printing cash.

Balance sheet is de-risking mechanically: debt stays basically flat wile assets balloon to debt/assets collapses. That’s important because it means NVIDIA can keep doing ecosystem bets and buybacks without becoming financially fragile.

1) What’s actually driving the stock right now

(A) The market has redefined the unit of demand from “GPUs” to “AI factories.”

On the call, management keeps hammering “compute equals revenue” and “tokens per watt equals dollars per watt.” That’s the economic logic of a power-limited world. It explicitly frames the data center as the new unit of computing and networking as integral to that stack .

(B) The business has become overwhelmingly “Data Center and networking attach.”

In FY2026, Data Center was $193.7B out of $215.9B total revenue (90%) . And inside that, networking was $31.4B (vs. $13.0B prior year) .

So the stock is now a referendum on (1) capex budgets, (2) time-to-power, (3) NVIDIA’s ability to keep bundling the rack (GPU+NVLink+switches+NICs+Ethernet/IB) and capture the “systems” margin pool.

(C) Supply visibility has become a fundamental input into valuation.

The market isn’t used to a semiconductor company effectively guiding “years” of demand visibility, but the financials show why they’re saying it: manufacturing/supply/capacity commitments were $95.2B (substantially paid through FY2027) . That’s a quasi-backlog signal… and also a leverage point if demand ever hiccups (more on that in risks).

(D) Price action is telling you “earnings are real, but the next leg needs a new proof point.”

On the chart, NVDA put in a big 2025 base (that yellow box) and then repriced higher, but the recent action is more of a high-level consolidation near the highs rather than a fresh impulse move. That’s classic when fundamentals are compounding but the market is waiting for the next catalyst: Rubin ramp timing, inference monetization confirmation, and the durability of hyperscaler spend.

2) The main prospects

Prospect #1: Inference becomes the dominant economic workload, and NVIDIA is positioned at the right constraint: performance-per-watt.

The calls most important shift is not “AI is growing,” it’s that agentic workflows drive token volumes that are directly monetized (coding agents running minutes/hours, teams of agents, etc.). In that regime, the scarce resource is not FLOPs; it’s power and utilization. If NVIDIA keeps winning “tokens per watt,” it wins the right-to-build.

Prospect #2: NVIDIA is pulling more of the rack’s bill-of-materials into its own P&L.

This is the underappreciated structural move: networking is no longer an accessory; it’s becoming part of the core platform economics. The 10-K calls out NVLink Fusion explicitly, enabling hyperscalers/custom ASIC designers to integrate custom CPUs/XPUs with NVIDIA’s platform . That’s a strategic wedge against the “hyperscalers will design you out” narrative: even if they customize compute, NVIDIA wants to remain the fabric and software layer that makes the factory run.

Prospect #3: Product cadence is being weaponized as a moat, but it has to be executed.

The earnings realease is explicit that Rubin is expected to commence production shipments in 2H of fiscal 2027 . The bull case is that NVIDIA has turned architecture transitions into a flywheel: every year you get a step-function in perf/watt, and customers treat that as a revenue unlock, not an optional upgrade.

Prospect #4: The cash engine is now big enough to influence the stock mechanically.

FY2026 net cash from operations was $102.7B and capex spending was about $6.1B, so “owner earnings” are enormous. They repurchased $40.4B of stock in FY2026 . In a sideways tape, buybacks matter because they quietly raise the floor under per-share compounding.

3) What will move the needle from here

Here are the catalysts that matter, ranked by “likely to hit” and that “market cares.”

Near-term (next 1–2 quarters)

1) Blackwell Ultra / GB300 ramp confirmation

The 10-K notes they began shipping production units of Blackwell Ultra (including GB300) in FY2026 Q2 .

What the stock wants is a clean ramp and no nasty margin surprises.

2) Networking continues to scale faster than compute

If networking keeps compounding anywhere near the FY26 pace (DC networking up massively to $31.4B) , the market starts valuing NVDA less like “a chip supplier” and more like “AI infrastructure prime contractor.” That is multiple-supportive.

3) Gross margin narrative stabilizes

FY26 GAAP gross margin dipped to 71.1% from 75.0% due to mix shift to full-scale Blackwell solutions + the $4.5B H20 inventory/purchase obligation charge .

What moves the stock is the market believing margins are structurally “mid-70s-ish” through the cadence, rather than “downhill as systems get complex.”

4) Buyback floor

They’ve got massive authorization and have been using it: board approved +$60B repurchase authorization (Aug 2025), FY26 repurchases were $40.4B, and $58.5B remained authorized as of Jan 25, 2026 .

In a choppy tape, this can matter more than people admit.

Medium-term (this year, into next)

5) Rubin timeline credibility

Rubin is expected to commence production shipments in 2H of fiscal 2027 .

This is huge: the stock will re-rate on confidence that the transition is additive (sell Blackwell and start Rubin) vs disruptive (pause/air-pocket).

6) NVLink Fusion “platform capture” becomes visible

If you start seeing more disclosures and partnerships where NVIDIA’s fabric gets adopted even alongside custom silicon, that’s a direct rebuttal to the bear case.

7) China clarity equals optionality

They disclose: H20 required a license, caused that $4.5B charge; later licenses allowed some shipments and they generated $60M H20 revenue under those licenses; H200 license exists but no revenue yet .

Any improvement is upside optionality. Any tightening is another headline risk.

4) The risks the chart is “pricing in”

This is where the “range” makes sense:

- Capex stops being self-funding: if ROI doesn’t show up in customer financials, the “compute equals revenue” story weakens.

- Transition execution issues: the company itself warns cadence and complexity can cause delays and volatility .

- Power/capital bottlenecks become the limiter: they explicitly say the availability of data centers, energy, and capital is crucial, and shortages can impact revenue .

- Concentration risk: those top customers matter a lot (22% and 14%) .

5) Distilled

NVDA is being driven by the market’s belief that “AI tokens are the new unit of GDP,” and NVIDIA’s edge is turning power into profitable tokens better than anyone, but the stock will only break out of this consolidation when investors see (1) durable capex funded by real ROI, (2) flawless platform transitions, and (3) continued expansion from GPU vendor into full-stack AI infrastructure company.

Leave a comment