How I Found It, And Why It’s Timely

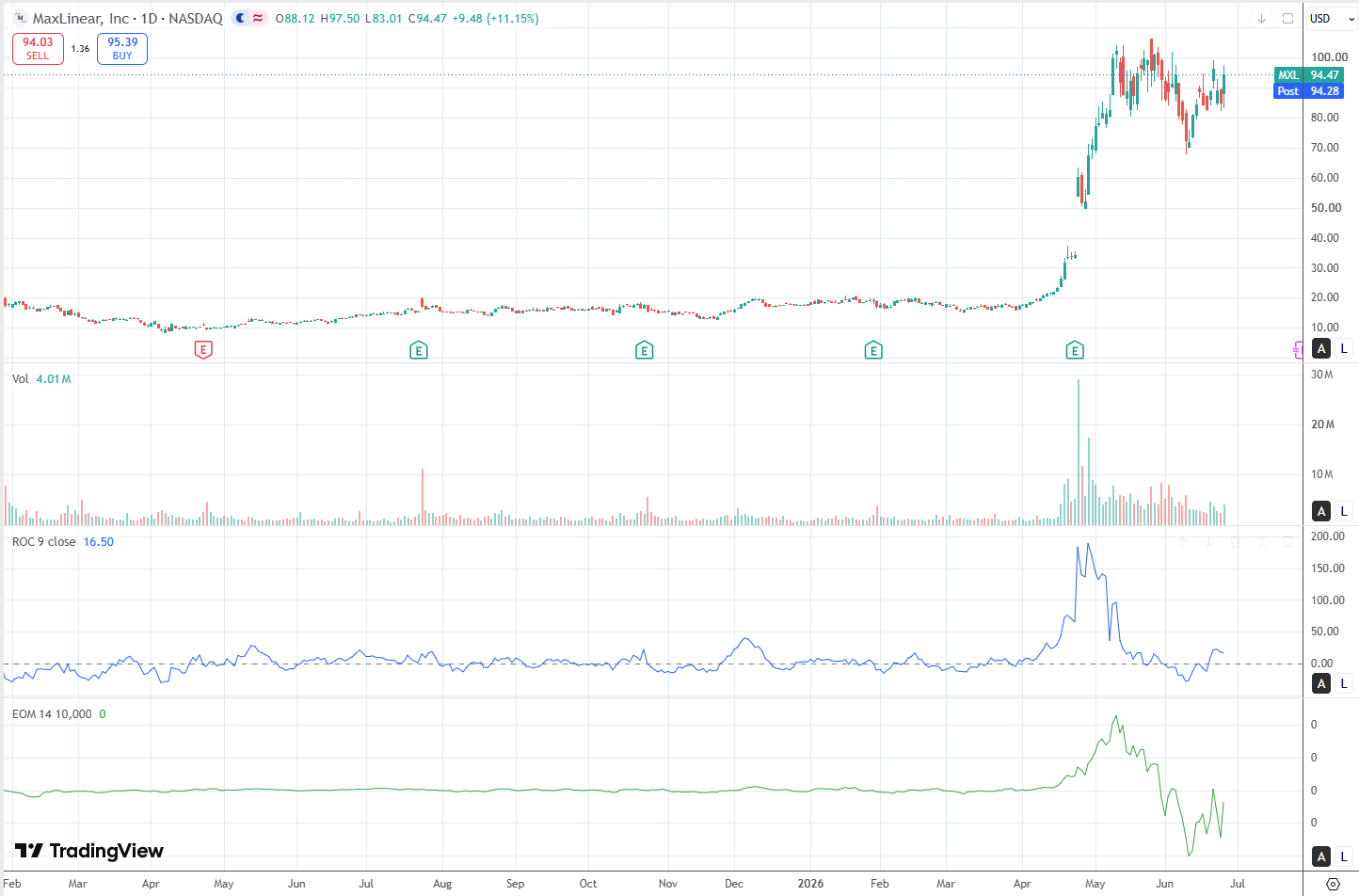

I didn’t start with the story; I started with the tape. MaxLinear (MXL) surfaced at the top of a momentum-breakout screen across the Nasdaq, a stock that had spent two years dead in the mid-teens and then exploded to ~$100 in a matter of weeks on a volume spike north of 30 million shares. A move like that, off a base that long, almost always means the fundamentals broke a long-standing range, not the chart. When I went to the filings, that’s exactly what I found: a beaten-down connectivity company that had reinvented itself as an AI optical-interconnect play, with the inflection landing in the most recent two prints. The breakout was the smoke. The optical data-center ramp is the fire. The problem is that the fire is now very visible, and the crowd has already paid up for it.

What The Chart Is Saying: The Breakout Already Happened

For roughly fifteen months, through March 2026, MaxLinear was a flat line in the $13–20 range, a long, dull accumulation base. The breakout fired in April and May: a near-vertical move from the mid-teens to ~$100–105 on a volume explosion north of 30 million shares in a single session. That impulse is now spent. Momentum confirms it: the 9-day rate-of-change spiked toward 190 at the May blow-off and has since collapsed to the mid-teens, and volume has steadily faded off the peak. That is the fingerprint of a post-breakout move, not an ongoing one.

What we have now is a fresh, very wide box building at altitude: a floor around $70 and a ceiling around $100–105, a range better than 40% wide, volatile, unresolved consolidation that will eventually declare itself as either re-accumulation (a bullish pause) or distribution (a top). At ~$94 the stock sits in the upper third of that box, below its highs. Even the most recent session, an eye-catching +11% day that swung from $83 to $97.50, is an intra-box bounce, not a breakout: it never challenged the ceiling.

This is why the chart and the fundamentals point to the same conclusion. At today’s price you get no technical edge: the fresh-breakout entry was in May, and the reset pullback hasn’t come. The two lines that would be actionable map almost exactly onto the valuation triggers below, a decisive close above ~$105 on expanding volume (continuation, the business growing into the move), or a test of the ~$70 box floor (the pullback entry, which lines up with the $60s–low-$70s level where the risk/reward resets). Until one of those prints, the tape says the same thing the numbers do: wait.

Business Overview: A Connectivity Castoff Becomes An Interconnect Company

MaxLinear designs RF, analog and mixed-signal chips. For most of its life that meant broadband and connectivity — cable and fiber gateways, Wi-Fi, the unglamorous silicon inside your ISP’s equipment. That business is brutally cyclical, and it showed: revenue collapsed from $693 million in 2023 to $361 million in 2024 as the industry worked off a post-COVID inventory glut. The stock got left for dead.

What the market missed is that, underneath the broadband bust, MaxLinear was building an infrastructure franchise, and the centerpiece is optical. Every AI cluster needs to move enormous volumes of data between GPUs and across the data center, and that traffic runs over optical transceivers. Inside each transceiver sits a PAM4 DSP, the chip that cleans up and drives the high-speed signal. MaxLinear’s DSP platform is called Keystone, and as of the latest quarter it is shipping at scale, at 400G and 800G, across multiple hyperscale customers in both the U.S. and Asia.

That changes the shape of the company. In Q1, infrastructure became the single largest segment at $63 million, up 136% year over year, eclipsing broadband ($44M), connectivity ($19M) and industrial/multimarket ($12M). And there’s a pipeline behind Keystone:

- Rushmore (a 200-gigabit-per-lane DSP) and Washington (its matching transimpedance amplifier) extend the platform to 1.6 terabit, with production ramps beginning late 2026 into 2027, and 1.6T carries higher ASPs and margins.

- Annapurna, a 1.6T active-electrical-cable and 3.2T onboard retimer family, opens the “scale-up” inside-the-server interconnect market that has minted Credo.

- Panther, a storage accelerator, is set to at least double revenue in 2026 as memory constraints make hardware-accelerated compression valuable.

- New footholds: a first XGS-PON design win at a hyperscaler (a dedicated control-plane network), USB bridge wins at two hyperscalers for rack management, and 5G radio SoCs.

The strategic point management keeps making is incumbency: shipping Keystone at scale, clearing the interop qualifications, proving it can supply, makes MaxLinear the incumbent the hyperscalers and module vendors trust for the next node. That’s real, and it’s why the 1.6T pull is arriving faster than the company expected.

The Bull Case: The Products That Can Actually Move The Needle

The inflection is visible in the headline numbers: revenue up 43%, infrastructure up 136% and now the largest segment, non-GAAP operating margin swinging positive:

| Metric | Q1 FY2026 | Q1 FY2025 | Change |

|---|---|---|---|

| Revenue | $137.2M | $95.9M | +43% |

| — Infrastructure | ~$63M | ~$27M | +136% |

| Non-GAAP gross margin | 59.5% | ~57% | +~2.5 pp |

| Non-GAAP operating margin | +16% | negative | inflected positive |

But a single quarter doesn’t settle a Hold-versus-Buy debate — the products behind it do. The bull case rests on a specific set of platforms and design wins, each with a defined path to revenue or margin. Here are the ones with the weight to matter.

Keystone (800G optical DSP): the revenue engine that’s already shipping. Keystone is the PAM4 DSP at the heart of the optical transceivers wiring AI clusters together, and it is in volume production today across multiple hyperscalers in both the U.S. and Asia, at 400G and 800G, for scale-up and scale-out. Management raised its 2026 optical data-center revenue target mid-cycle to $150–170 million — up from roughly $130M — which by itself takes optical from a rounding error to roughly a quarter of total revenue. Just as important as the dollars is the incumbency: clearing the hyperscalers’ interop qualifications and proving it can supply at scale makes MaxLinear the trusted vendor for the next node. That is the moat the whole thesis leans on.

Rushmore and the 1.6T transition: where the ASP and margin uplift live. Keystone is 800G; the money in optical is migrating to 1.6 terabit, and MaxLinear’s answer is Rushmore (a 200-gigabit-per-lane DSP) with its matching Washington TIA. Production ramps begin late 2026 into 2027 — and this is the higher-margin leg, because 1.6T parts carry richer ASPs. Management was explicit that the mix shift toward 1.6T has “an uplifting effect on revenues and gross margins even as market share expands.” Keystone’s success is de-risking Rushmore directly: incumbency is pulling 1.6T engagement forward faster than the company expected. This is the second growth leg, and it lifts margin while it lifts revenue.

Annapurna and Washington: the scale-up adjacency that widens the TAM. Optical DSP is one market; MaxLinear is using its physical-layer engineering to step into the next. Annapurna is a 1.6T active-electrical-cable and 3.2T onboard-retimer family for scale-up — the inside-the-server interconnect market that has minted Credo, and which management calls “humongous as speeds increase.” Washington, the TIA, is a fundamental building block for LPO/LRO and co-packaged-optics architectures and can attach to other vendors’ DSPs — pure optionality. Management’s own TAM ranking tells you the order of the prize: #1 optical transceiver DSP (overwhelming the rest), #2 electrical retimers, #3 AECs. Together these turn MaxLinear from a single-product optical story into an interconnect platform.

Panther: the non-optical vector that doubles in 2026. Panther is a hardware storage-accelerator SoC, and management guides its revenue to at least double in 2026. The tailwind is memory: roughly 60% of data-center spend is memory, and as AI scales, low-latency, high-capacity memory access becomes the bottleneck. Panther accelerates exactly that — compression, throughput, latency — and is migrating from enterprise storage appliances into mainstream cloud deployments, with Panther 5 already sampling. It is a second, independent compounder that doesn’t depend on the optical ramp.

XGS-PON and USB bridge wins: small today, content-per-rack optionality. MaxLinear secured its first XGS-PON design win at a U.S. hyperscaler — a dedicated, resilient control-plane network spanning data centers, a use case management sizes at “hundreds of millions” of TAM, ramping in 2027 — and won USB bridge controllers at two hyperscalers for rack-level system management. Each is small now, but both expand MaxLinear’s dollar content inside every rack. That is the land-and-expand mechanic that turns a chip vendor into an infrastructure supplier.

The margin half of the story. These initiatives move gross and operating margin, not just revenue, through three levers: infrastructure and optical carry structurally higher gross margins than legacy broadband, and the mix is shifting fast; 800G-to-1.6T is richer still on ASP and margin; and operating leverage is real. Q2 revenue steps up 18–24% sequentially on roughly flat operating expense, which is how non-GAAP operating margin already reached 16% and can keep climbing. The honest near-term offset, which management flagged itself, is rising wafer and packaging input costs, the reason gross-margin guidance (58–61%) stays cautious even with the mix tailwind.

The Valuation: Why This Is A Hold, Not A Buy

Source: YCharts

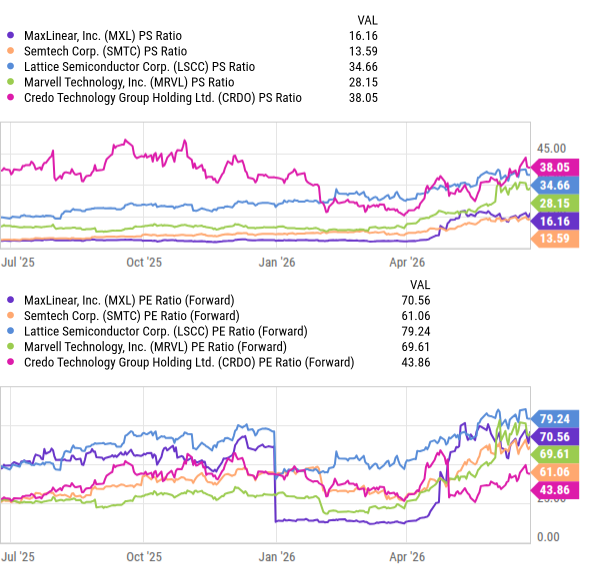

The strongest bull argument is relative: against the cohort it now competes with, MaxLinear screens as the cheapest interconnect name on sales — roughly 16x trailing sales versus Credo at ~38x, Lattice at ~35x and Marvell at ~28x. The market has started to concede MaxLinear belongs in this group but still won’t price it like a member, and if it simply re-rated halfway toward the cohort, the stock works without heroics on out-year numbers.

Here’s the catch, and it’s the whole reason I stop short of Buy. “Cheapest on sales versus Credo” is a relative statement. On an absolute basis, MaxLinear at ~$94 — an ~$8.4 billion market cap — trades at about 13x forward 2026 sales and ~50x forward 2027 earnings. That is not a cheap stock. It is a less-expensive expensive stock.

I value MaxLinear on sales rather than earnings, because GAAP earnings are still distorted by heavy stock comp and acquisition amortization (the company posted a GAAP net loss in Q1 even as non-GAAP operating income turned positive). I project revenue to year-end 2027, divide by a forecast ~96 million shares, apply a bull and a bear exit multiple, and solve for the return from today:

| Scenario | FY2027E Revenue | Shares | Revenue / Share | Exit P/S | Implied Price | Total Return |

|---|---|---|---|---|---|---|

| Bull | $850M | 96M | $8.85 | 15x — re-rates halfway to the interconnect cohort | ~$133 | +41% |

| Bear | $620M | 96M | $6.46 | 4x — de-rates to the cyclical-semi multiple it carried for years | ~$26 | −72% |

The base case is the tell. Put the Street’s ~$792 million 2027 revenue on a roughly-unchanged ~12–13x multiple and you get ~$99–107 — within shouting distance of today’s price. In other words, at $94 you are already paying for the consensus to come true. You make money only if the beats keep coming (the bull), and you lose badly if the optical ramp slips even a quarter or two and the multiple snaps back toward where this cyclical name has traded for most of its life (the bear).

That is a fundamentally different shape of bet than a cheap stock with a catalyst. The upside is real but capped by the multiple already paid; the downside is a 60–70% air pocket. I don’t take balanced-to-negative skew on a momentum chart, however good the story.

Risks

These are specific, not boilerplate:

- It’s priced for the beats to continue. After a ~6x run, the base case is in the stock. Any quarter where optical disappoints, wafer costs compress margins, or guidance merely meets rather than raises, and a 13x-sales / 50x-earnings momentum name de-rates fast — the bear lands near $26.

- Customer and program concentration. The ramp leans on a handful of hyperscalers and module vendors. Management admits it is “only halfway” to diversifying across end data centers. Concentrated ramps cut both ways.

- It’s the small fish in a shark tank. MaxLinear competes with Marvell and Broadcom — vastly better-capitalized — and with Credo in AECs. It exited Q1 with only ~$61 million of cash against $125 million of term debt and negative operating cash flow (large wafer prepayments). The balance sheet is thin for the capital intensity of this ramp.

- Dilution is real. Share count is rising (≈89.5M to ~95M diluted) on heavy stock comp; a $75 million buyback authorized in late 2025 only partly offsets it.

- The cyclical core hasn’t fully healed. Broadband and connectivity are recovering off a deep 2024 trough, and DOCSIS 4.0 timing keeps slipping. If infrastructure stumbles before the legacy base re-accelerates, there’s no cushion.

Conclusion

MaxLinear is the rare turnaround where the transformation is genuine: a broadband castoff has built a real AI optical-interconnect franchise, Keystone is shipping at scale across multiple hyperscalers, the next-generation 1.6T pipeline is pulling forward, and estimates are rising rather than falling. The business deserves a Buy.

The stock, at ~$94, does not — yet. A six-bagger has already discounted the consensus case, and the risk/reward from here is balanced-to-negative: roughly +40% if the beats keep coming against −70% if the ramp slips. I rate MXL a Hold, and I’d flip to Buy on either of two triggers: a pullback toward the $60s–low-$70s, where the bull/bear skew turns clearly positive again, or another beat-and-raise that lifts 2027 numbers ~15%+ and lets the company grow into its multiple. This is a name I want to own. It is not a price at which I want to buy it. With a stock this volatile, that price tends to come.

Disclosure: I have no stock, option or similar derivative position in any of the companies mentioned, but may initiate a beneficial Long position through a purchase of the stock, or the purchase of call options or similar derivatives in MXL over the next 72 hours. This text expresses the views of the author as of the date indicated, and such views are subject to change without notice. The author has no duty or obligation to update the information contained herein. Further, wherever there is the potential for profit, there is also the possibility of loss. Additionally, the present article is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Some information and data contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. The author trusts that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.

Leave a comment