Summary

- There’s too much emphasis on cash flow statements, and financials in general, when evaluating Tesla.

- The mismatch between current operating cash flow and Capex for the Model 3 make it impossible to understand the current state of affairs using just financials.

- Philip Fisher used scuttlebutt techniques. The internet has taken it to a whole new level.

- Musk’s biography and technical blogs offer better information about how Tesla will get out of its production hell.

Valuing Tesla (NASDAQ:TSLA) is a troubling exercise. Many of the analysts have taken the discussion to the personal level. For most, Musk is either a genius or a fraud, there’s no middle way. Make no mistake, this kind of polarized view has happened in the past, in many stocks.

In part, this is fueled by the theoretical financial background of many analysts. They tend to look at stocks as rigid securities with a couple of variables (growth rate, margins, dividend yield, etc.) that will not change in unpredictable ways. Therefore making it possible to forecast future cash flows with a good level of confidence.

This idea was first introduced in The Theory of Investment Value by John Burr Williams. In a world without uncertainty, investors would only get “equity bonds” – very predictable cash flow institutions with some degree of growth. Don’t be fooled, those kinds of securities are the exceptions rather than the rule.

Nevertheless, the discounted cash flow is a pretty good technique to evaluate established companies with stable processes and in mature markets. However, it won’t work with growth stocks.

For this last group, I recommend reading Common Stocks Uncommon Profitsby Philip Fisher. Although it is an investment book, I don’t recall any of the usual mathematical apparatus. There is a good reason for this: as the name tells, to hit a profitable growth stock you need to get right the assumptions about… well, growth and margins! And for that, you need more than a spreadsheet with a couple of discounted cash flows. There’s no merit in it if the assumptions are wrong. That’s why Philip Fisher focused on the methods to get a good grasp on the assumptions about growth and margins. (I am simplifying Fisher’s investment philosophy – there’s a lot into it, and if you want to know more, you should definitely read the book.)

Tesla is a growth stock

Tesla falls under the growth category. Many will argue that it is not even a growth stock because the company can’t deliver on its production targets, etc. Well, that’s just nonsense. EVs and autonomous driving are promising fields and Tesla is present in both, building more cars every year. Most likely, the market for EVs will grow at the expense of internal combustion vehicles, which gives it enormous space to grow. A bit like the smartphone market that expanded at the expense of the feature phone market.

On another perspective, Tesla is trying to ramp up production to a scale only matched by its own valuation. The ambition to reach half a million of cars by 2018 makes it a meaningful car player in the auto industry. If this materializes, Tesla’s growth rates between its IPO until 2018 will be fantastic, and its current valuation totally justifiable.

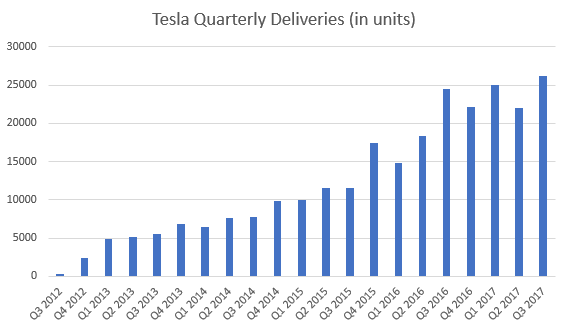

Graph 1 – Tesla Quarterly Deliveries

(Source: Graph made by the author based on data from statista.com)

Now, returning to reality, the ramp-up process implies that the tooling expenses are huge. We can have infinite arguments about Tesla’s cash burn rate. However, the pivotal point is that the cash is being spent now, while the cash flow from those investments will enter the company during the following years.

Obviously, since Tesla is only getting cash inflow from 80,000 cars per year, but it is spending on the capacity to build 500,000 cars, the mismatch here is huge. Therefore, it is easy to say that since the company is hemorrhaging cash, it is performing badly. However, this is misleading. Financials, especially cash flow statements, are not a good proxy for Tesla’s future performance. In the end, it all comes down to growth and future margins, and presently, none of those are well-represented in the books.

Musk’s biography is a better predictor for growth and margins than financials

Going back to Fisher, the internet has rendered some of his scuttlebutt methods old. Nowadays, you can go to Seeking Alpha and get technical expertise on one sector or get transcripts with Q&As with the management team. You can check a TED talk or order a book online about one of those entrepreneurs that claim to be shaping the future. Or even follow one of those obscure blogs with an incredible track record on getting accurate information on some sector or company. Basically, Philip Fisher’s principles are still valid, it’s just that you can use other means.

In Musk’s case, his celebrity-like status makes him highly notorious and the target of many reporters. Therefore, it isn’t hard to find a book about him. And that’s precisely what I did.

I’ve read Ashlee Vance’s book on Elon Musk, and this is a very good piece of work. The episodes he recounts are so vivid that you can really grasp the way Musk tends to work around problems and the results he has accomplished so far. And more precious than that, you can get a good idea of how he will act going forward.

3 relevant Muskian thinking patterns

Firstly, Elon Musk is always looking for opportunities to ditch current consensus and kick-start a paradigm shift. One good example was the online bank x.com, later PayPal.com. Everyone thought the barriers to entry were huge, but Musk was attracted by his perception that complacency was reigning in the banking business. Since he was one of the first internet millionaires, he knew that the web had the potential to revolutionize the banking business.

Secondly, he explores his ideas through non-conventional ways. PayPal is again a good example. Back in the ’90s, starting an online bank was something unheard of. Confidence is one of the most important assets in the banking business. Most players feared that consumers would never get confident enough to adopt online banking, but Musk was eager to explore this route.

Finally, most of the time, Musk will be wrong about his initial ideas (and deadlines). But he will be glad to get it wrong in order to get it right. PayPal is an online payments system, not a bank, which was the initial idea. After all, entering the banking business wasn’t that easy. Therefore, he changed tactics and decided to take a smaller step by getting entrenched in the payments segment of the banking market (he still wanted a full-fledged bank, but PayPal was sold before that could happen).

Growth case: Musk likes ditching consensus

Before SpaceX showed that was possible to put things in orbit using an in-house produced rocket, everyone assumed that space-related ventures were reserved for powerful nations. Again, the complacency was so big that Musk felt compelled to investigate the sector economics.

He thought about sending mice to Mars just to reignite the appeal and interest in space travel. He even thought about committing up to $50 million to the cause. However, when he sought out quotes for rockets from the ULA (United Launch Alliance), a joint venture between Boeing (NYSE:BA) and Lockheed Martin (NYSE:LMT), he was asked for more than $60 million per rocket. It was way out of his budget.

He then tried the Russians, and they asked for $15 million. It was still too much. He had found the critical point: rockets were too expensive. The solution: do it yourself! At that point, Musk started with one of the key elements of his industrialist career: vertical integration. Believe it or not, but in an age where outsourcing is the mainstream of management theory, vertical integration has been giving SpaceX a competitive edge.

SpaceX’s initial business model was building small rockets that could be used to put satellites in orbit for companies at lower costs than the ULA. Now it is transportation of supplies to the International Space Station, and in the future it might very well be taking people to Mars. This is growth by ditching consensus.

Margins case: How SpaceX reduced costs

The recipe was simple: it avoided legacy designs, did as much as possible in-house, and avoided bureaucratic supply chains, layers of contractors and cost-plus contracts – all features that plague SpaceX competitors.

Some episodes are almost comical. For instance, when sourcing for a complete computer system for the rocket’s avionics, the quotes were all for around $10 million. Musk asked a small group of engineers to build it themselves using standard computer parts and developing the rest. One year later, they had a concept system costing $10… thousand!

How Musk’s track record contributes in Tesla’s financials

Musk’s willingness to ditch consensus is a strong indicator that his ventures never stop short of ideas to get new things to market. This is reflected in the fact that Tesla started as a silly idea to put an electric motor into a Lotus chassis, and the company is now trying to develop an autonomous truck that has the potential to endanger the establishment in the trucking business.

Therefore, a lack of ideas to increase sales does not seem to be a problem. Another factor that as always characterized Musk’s companies is that their product ideas always seem to resonate with the consumers a lot sooner than the companies can deliver the actual products.

On another front, the 25% gross margin goal has been regarded by many analysts as unattainable. Let me disagree with you. The examples I’ve provided about SpaceX’s cost reduction prowess should be an indicator of what Musk is capable of. He is always eager to ditch consensus, and he will always go after the big costs in the process. That’s why he has decided to take battery production in-house, which is one of the biggest costs of the EV. Musk is capturing all the benefits from the learning curve to have a cheaper and better product earlier than competition.

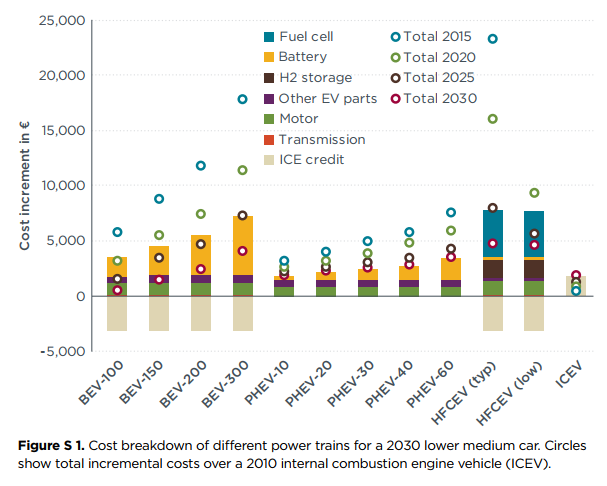

Graph 2 – Breakdown of incremental costs over ICEVs

(Source: International Council on Clean Transportation)

Wonderful story! Can you put it into numbers?

So far we have seen that even if Musk fails his own deadlines, he has, sooner or later, delivered something close to his initial claims.

Delivering on the Model 3 will be a function of time. In business, time is money, so it all comes down to whether Tesla will have enough cash until it can set up a stable operation for the Model 3. We’ll explore that later.

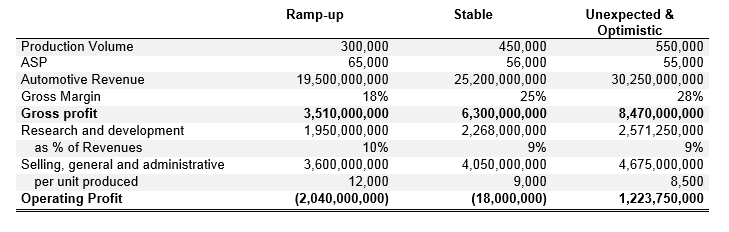

I’ve tried to come up with three scenarios for the production process in the company’s automotive division. The idea is to divide the production into 3 phases. In the 1st one, there’s a production ramp-up and a pretty much chaotic process, then we will have a stable process, and finally, the learning curve will kick in and bring unexpected gains. By unexpected gains, I mean more production and lower costs than expected, diluting quasi-fixed SG&A expenses by more production units.

Table 1 – Sensitive analysis to Tesla’s learning curve in the Automotive unit

(Source: Author estimates based on Tesla’s 10-K)

This simplistic model tells us that the single most important factor is the gross margin, i.e., the production process. As we have seen, SpaceX has seen incredible cost reduction through re-engineering, redesign and vertical integration. That’s the same approach that Tesla has been applying to its automotive division. The problem is that, unlike SpaceX, Tesla is producing thousands of cars bearing up to 4000 individual components. Hence the delays.

Looking at Table 1, we can see that the optimistic scenario is the only one that investors seem to be discounting. The current operating multiple would be unjustifiable if expectations pointed to the stable scenario. Investors are discounting the optimistic scenario and the growth to come from the Semi, Roadster and Model Y.

Basically, investors are divided into those who believe Tesla will be in an eternal ramp-up (shorts) and those who believe the optimistic scenario for the current operations is just around the corner (longs).

Musk is a genius, but there’s got to be a weak spot!

Yes, there is: cash.

This might seem contradictory, since I’ve said that the cash flow statement is not a good proxy for Tesla’s future operating performance. However, I didn’t say it isn’t a good way to evaluate the present risk of a cash constraint. The company is indeed spending money at a huge rate.

The decision to issue bonds instead of raising more capital at a moment when the stock price was sky-high might have been a mistake. Tesla has grown so ambitious that cash management seems just another nuisance on the way.

Historically, when the word spreads that a company is facing a cash shortage, this tends to be a self-fulfilling prophecy. And Tesla’s management should know better – the company barely escaped one.

If the production bottleneck keeps delaying the entry of cash flows from the Model 3, Tesla will most likely need another capital raise in the short term. However, that implies a streak of bad news, and at that time, the stock might be much lower than it is today. If that happens, the dilution will be higher for current shareholders.

How to approach the current production hell from an investor’s standpoint

Presently, I think Tesla is in a very competitive arena and traditional automakers are not standing still. However, it seems to me that Musk’s drive and the company’s horizontal structure offer execution speed and out-of-the-box solutions that other automakers cannot match. Make no mistake, what Tesla has achieved so far is heroic. In the auto industry, going from around $1 billion to $60 billion market cap in 10 years is exceptional. In that context, the current production hell might just become its biggest strength.

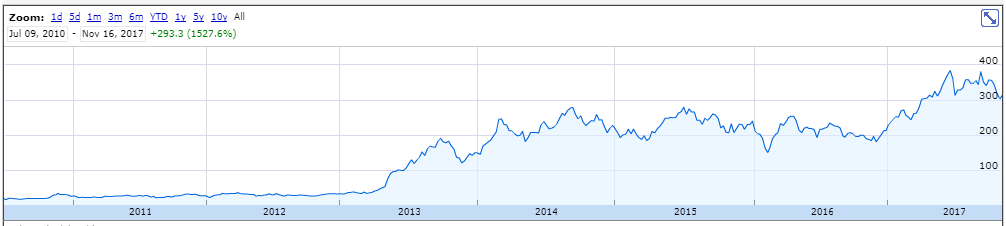

Graph 3 – Tesla stock price since its IPO

(Source: Google Finance)

That said, there are short-term risks related with operations that will influence cash management and might cause negative outcomes in the following 12 months.

The company’s strategy implies that until the Model 3 operations are stabilized, more capital will be necessary. However, the Tesla Semi and, most importantly, the Tesla Roadster 2.0 will be money makers. The company has come a long way from having zero manufacturing experience and trying to produce half a million cars. The first Roadster was plagued with problems, and its manufacture was far from being top-notch. The second version of the Roadster will be a huge leap from those early days. Above all, it has the conditions to be a money maker – the icing on the cake. The catch is that the Roadster is still years away.

Bearing that in mind, I think a lump sum investment should be avoided in the present. The Roadster 2.0 is still years away, and the Model 3 operations are still not stabilized.

You can follow two approaches to enter this stock. Stay on the sidelines until there is sufficient evidence that the company can solve the production problems and stabilize the process. The downside of this approach is the fact that as soon as it becomes widely known that Tesla is catching up on production, the stock will soar and you might miss the initial move. However, the long-term potential should offset the loss of knee-jerk reaction to a set of good news.

Another strategy is dollar-cost averaging during the next 12 months. This will provide both exposure to the stock and a cushion to absorb further negative news. Be disciplined and regularly reevaluate the investment thesis to incorporate developments capable of changing the future of this stock.

What I think you should not do is short the stock. There is a great article on Seeking Alpha titled “Why Good Shorts Go Bad…” There you can get a good grasp of the conditions necessary for a successful short. It suffices to say that although the short term might push the stock down, I do not think all the conditions are met to have a successful short.

I’ll just mention two important questions. Who’s on the other side of the short? Namely, who is supporting the stock, or who might jump in to save the day? And is there a clear catalyst that might change the psychology of the investors? In my opinion, the answers to these questions lie in a clouded area, and therefore, it is extremely hard to be precise about how the short would work. This is not to say you cannot make money shorting the stock, it just means it is hard to do so consistently. We all have seen Tesla soaring on bad news… the stock has been a short trap.

—

Disclosure: I/we have no positions in any stocks mentioned, but may initiate a long position in TSLA over the next 72 hours.

Note: This article was originally published on seekingalpha.com

Leave a comment