Since the Iran war began, the market has behaved like it usually does in a realtime stress test: it paid up for protection first, then began to withdraw that payment once the worst-case path didn’t continuously intensify. The clearest message is that the “war hedge” complex (oil, energy equities, even gold) has stopped acting like the only game in town, while broad equities, particularly tech/growth, have resumed leadership. That doesn’t mean the war is irrelevant. It means the marginal buyer is no longer willing to pay an ever-rising premium for it.

My approach here is simple: dont argue the headlines. Watch what stops working. When the hedge stops working, the next money is often made in the reversal, owning what the hedge was suppressing, until the tape tells you the war premium is back.

1) The setup: shock hedges worked, then they didn’t

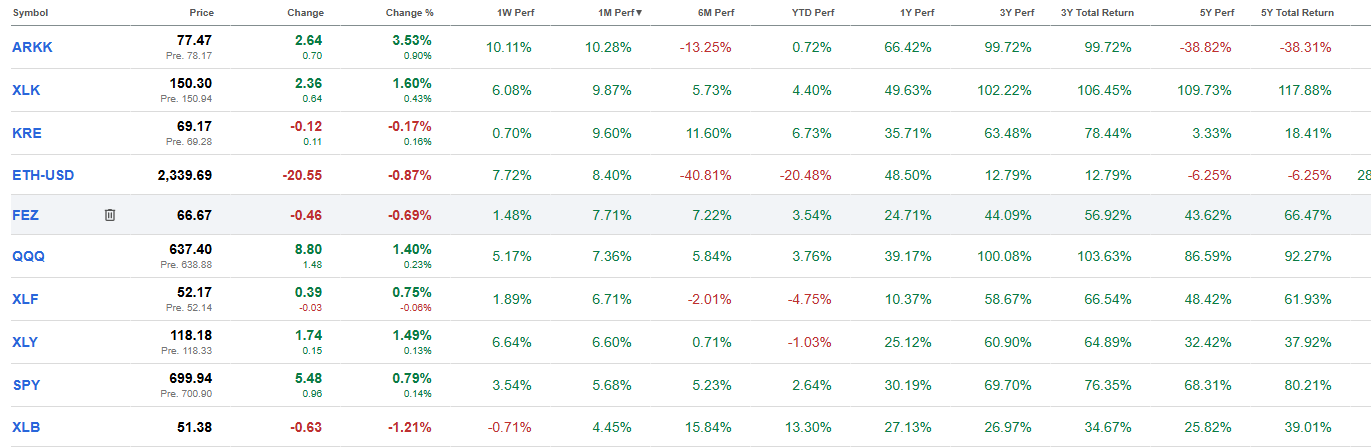

In the rearview, the market clearly treatd the conflict as a real constraint. Oil and energy are still massively positive on the longer windows: crude is up big over 6M and YTD, and energy equities have held strong returns as well. That’s the signature of a market that initially priced disruption risk into the commodity complex and into the sectors most levered to it.

Source: Seeking Alpha

But the more important information is what’s happening now. Over the last month and week, crude is down, and XLE has softened on a 1M basis even though it remains strong over 6M/YTD. At the same time, risk is reappearing in places it typically doesn’t if the market believes it’s entering a durable oil-shock regime: QQQ and XLK are strong over 1M, SPY is firm, and even higher-beta expressions (ARKK) and cyclically sensitive segments (KRE) show meaningful 1M strength.

Source: Seeking Alpha

That combination, “crisis winners rolling over short-term while broad risk strengthens,” is the market’s way of saying: the shock was real, but the premium is being monatized.

2) The lie detector: crude’s reaction function

In geopolitical episodes, crude is the closest thing you get to a lie detector because it sits at the intersection of psychology and real-world constraints. The key question is not whether oil is high or low. Its whether it can continue to rise in response to bad news.

Over the last month, crude has struggled to sustain the bid. That matters because crisis pricing has a specific feel: oil grinds higher on any hint of escalation, volatility stays sticky, and equities either struggle or narrow. When that pattern breaks, when oil stops rising despite the story still being “serious” it often signals that the market has moved from panic pricing to probability weighting.

This is my main point: the edge isnt predicting the event; it’s recognizing when the markets reflex has changed. The reflex shift is what creates reversals.

3) Why this is an opportunity set, not a prediction

We didn’t need to forecast peace or escalation to make money. We needed to know what the market was already discounting and when leadership was rotating. Right now the market appears to be discounting a world in which the conflict remains a risk, but not one that continuously worsens into a sustained supply shock. That is why the war hedge complex can be strong on long lookbacks yet weak on the tactical windows, while equities broaden.

In other words, the opportunity is not war ends. The opportunity is the premium stops expanding. Those are very different trades. One is narrative. The other is tape.

4) The playbook: where the asymmetric trades tend to live

If the market is actively unpricing the war premium, the cleanest tactical expression is to fade the hedge and own the beneficiaries of easing fear. In practice that often looks like rotating away from energy beta and into growth leadership, sometimes explicitly via relative trades (energy vs tech), sometimes implicitly by trimming the hedge exposure and redeploying into the leaders.

The discipline is conditional. You don’t press that view because you feel clever; you press it because the market is telling you that the hedge is no longer being reinforced. The confirmation comes from relative strength: if XLE continues to lag SPY/QQQ and crude fails to reclaim momentum, the unwind can persist longer than feels comfortable. Thats typically how these reversals pay. Keep an eye on software stocks that were destroyed during the Iran affairs.

At the same time, it’s important not to confuse “oil fade” with “capex fade.” Even if crude meanreverts, the second order consequences of conflict, security priorities, energy independence, infrastructure build-out, can remain structurally supportive for certain pockets of the market. This is where a Druck-style framework becomes powerful: separate the headline trade (war hedge) from the structural trade (persistent investment cycle). It’s entirely possible for oil to cool while the “picks and shovels” of the buildout remain bid because the world doesn’t unlearn the lesson of vulnerability overnight.

That’s the subtle opportunity: fade the crowded hedge while keeping exposure to the longer duration beneficiaries of the new constraint set.

5) What would change the thesis quickly

This framework is only as good as its invalidation rules. The fastest way to be wrong is for crude to reassert itself, not with a one-day spike, but with a decisive breakout that holds and re drives energy leadership. If oil starts making higher highs and sustaining them, and if energy equities reclaim leadership versus the broader market, the tape is telling you the war has returned as a binding macro constraint. In that world, the reversal trade ends, and you rotate back toward protection.

On the other hand, if crude remains heavy despite continued headline noise, and equities keep broadening, with cyclicals and other higher-beta segments participating, the market is effectively confirming that the premium is being sold and that risk is being repriced higher.

The key is to treat crude behavior as the signal, not your interpretation of the news.

6) Portfolio posture: a two-speed stance

The most sensible posture in this kind of tape is a barbell that respects both realities. Tactically, you lean into the leadership rotation as long as the war hedge continues to fail: growth and quality risk can work if the market keeps un-pricing tail fears. Structurally, you maintain exposure to the capex and security implications that dont vanish just because the front-month premium comes off. That’s how you avoid being right about oil and wrong about the world.

Tou are not trying to be an oracle. You are trying to be positioned where the market’s odds are improving, and you are trying to exit quickly when the market tells you those odds have changed.

Closing thought

The most important pattern since Feb 28 isn’t that war caused X. It’s that the market absorbed the shock, paid aggressively for hedges, and is now selectively withdrawing that payment while re risking into leadership sectors. That shift from reinforcement to failure is where reversals and opportunity typically emerge.

Leave a comment