Prologue

In the semiconductors industry we are frequently watching old known producers facing increasing pressure. This is very recurrent, mainly, due to the characteristics inherent to the industry. The fact that the industry does not demand a prohibitive amount of capital for entry purposes makes it very attractive for newcomers. If we add a short life cycle for products, of about 1 to 2 years, this ends up being the recipe for a very competitive landscape.

Intel

Currently, Intel Incorporated (INTC) is one of those producers under pressure. The rise of the “super phones” along with the development of hybrid portable devices called “tablets” both with fabulous processing capabilities able to rival with portable computers, have opened new markets for the chipset industry. Seen as an unrivaled company in the portable and desktop computers, Intel has been pushed back to a small position in the mobile phone and tablet market. If we add the perception that the portable and desk computer segments are old markets poised to fade away, we get the main reasons why Intel’s PER, around 13, is not discounting much growth.

In this case, we are analyzing a company during an outlook crisis, which is raising concerns about the safety of the investment. Therefore, we should focus on correctly analyzing the safety of the company as a common stock investment target. Let us start by introducing the company’s organization. Intel is divided in five main operating segments (Source: Intel Financial Reports):

PC Client Group

This unit develops and sells products for notebooks and desktop computers destined at consumers and enterprise segments. The key success factors, in this segment, are to provide technological solutions that allow the development of thinner, lighter and smaller devices while improving battery life. The revenues provided by this operating segment represents 63% of the total revenues, while providing operating profits around $13,106 Million.

Data Center Group

This segment focuses in high performance cloud computing services and storage solutions. One key success factor is to provide a reliable service while being energy efficient. This division contributes for 21% of the company’s revenue, which corresponds to an operating profit near $ 5,020 Million.

Other Chips Architectures

This division includes products designed for mobile communications like netbooks, tablets and smartphones. One key element for the company’s success is to provide solutions for a wide range of operating systems. Intel has been able to get around 8% of its revenues from this segment, while posting an operating loss around $2,445 Million. Intel has been seen as lagging in these markets while, at the same time, the mobile devices market has become increasingly important for chipmakers, which constitutes a shift from the traditional PC market.

Software and Services

This operating unit develops software that can be used across all Intel based platforms. Intel is engaged in improving internet security through its McAfee division. The services have a weight around 5% on the company’s revenues while providing non relevant operating profits, around $1 Million.

Non-volatile Memory Solutions plus All other

The most prominent division from this group offers NAND flash memory products, representing 3% of the group’s total revenues. Together, the companies in this segment sum an operating loss around $2,256 Million.

The main picture that I take from this analysis is the fact that the PC Group division is providing 72% of the adjusted net profit; the Data Center division provides around 28%, while the Mobile Phones segment is a drag to the company’s earnings. My first conclusions led me to believe that the Data Center operations are being overlooked, since Intel is a first mover in this segment. The Data Center, alone, has the potential to more than replace the potential loss of revenues and profits in the PC Group in the coming years.

Production Operations

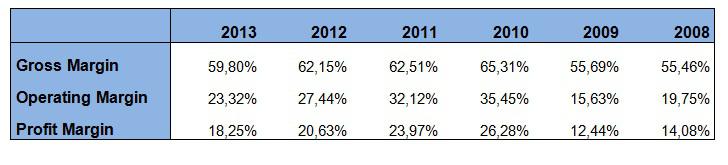

This is a determinant dimension, since the company is a manufacturing company. One good way to understand the company’s ability in this field is to look to the operating and profit margins of the last 5 years. Usually, these measures are a good way to understand what is happening in the production operations (Source: Reuters).

Table 1 – Gross, Operating and Profit Margins

By looking to the previous table, you can easily see that the margins achieved by Intel, in the last 5 years, are at an excellent level. These margins are the result of above average production facilities and premium products that allow for a high degree of differentiation.

Research, Development and Marketing

Intel has employed an average of $10 Billion in R&D in the past 2 years (Source: Intel Financial Reports), which is an average of 20% of sales. Intel has been doing this in order to develop new chips for new applications. One of the new markets, where the company is trying to enter, is wearable technology like the Google Glass. In this context, Intel is developing a line of processors called quark aiming to be one of the first movers in this market. This new line of products open a wide range of possible applications, from medical applications to public infrastructures, the possibilities are immense.

At the same time, Intel is trying to understand the change happening in the PC’s and mobile industries. The company was late to mobile phones and, now, is having a hard time penetrating a market where Qualcomm is well entrenched.

In the PC front the company is trying to develop faster and thinner processors that have reduced power consumption. At the same time, the company is also committed with server technology, data centers and data storage. Altogether this means that Intel is actively committed with continuously bringing new products to market in order to keep growth on the right track.

At the core of success it is always innovation. The challenges are provided by marketing intelligence from every sales point in Intel sales organization. Later the R&D department focuses in solving these challenges while interacting with the manufacturing organization, which is an area where I believe that Intel holds a big advantage against competition. The company makes sure that the researchers are placed near development plants that allow a fast experimentation of new ideas.

Financial Robustness

So far the company evidences very good features related to its operations. However, we should assess the balance sheet health.

Table 2 – Balance Sheet Ratios

Looking to the financial ratios, we get the idea that the company holds a solid position. The most liquid assets cover 1.48 times the current liabilities, while the current assets cover 2.36 times the current liabilities. Therefore, it is not predictable that any short term rupture will occur. Looking into the long term, the company evidences low leverage and a low level of debt in relation to the assets. However, the debt has been growing in the recent times, which prompts the idea that the company’s position has been degrading. My opinion is that Intel has been investing a lot more in R&D in order to accelerate some of its products to market, which the company has been doing, partly, through the emission of new debt.

Conclusion

Based on the overall picture described in the previous paragraphs, I believe that Intel is a long term growth play for a 3 to 5 years horizon. The company is very solid, has a good track record of innovation and problem solving, has state-of the-art resources, and a huge war chest.

Leave a comment