The most interesting innovation stocks are rarely just “growth stocks.” The best ones twnd to sit at a point where a system is being forced to change architecture. That is the key question with Navitas Semiconductor.

For years, Navitas was mostly understood as a GaN power semiconductor company with exposure to mobile chargers. That was interesting, but not enough. Mobile chargers were a good proof-of-technology market, but not a great long-term investment arena. The product could become smaller, faster, and more efficient, but once the charger was “good enough,” the market naturally moved toward commoditization.

That is what Navitas is now trying to escape.

The company is attempting to reposition itself from a mobile GaN story into a high-power infrastructure semiconductor company exposed to AI data centers, grid infrastructure, performance computing, and industrial electrification. In other words, the thesis is no longer about making consumer chargers smaller. The thesis is about whether AI infrastructure runs into a power bottleneck so severe that the entire power-delivery architecture has to change.

That is where the stock becomes interesting.

The core thesis: AI is not just compute-constrained; it is power-constrained

The market has already learned to price the first layer of the AI buildout: GPUs. Then it began to price the second layer: HBM, networking, and advanced packaging. But the next bottleneck is increasingly physical. AI clusters need power density, efficiency, grid access, and better conversion architectures.

That is the layer Navitas wants to own.

The CEO’s message is very clear: AI data centers and grid infrastructure are not separate markets. They are two sides of the same constraint. You cannot deploy hundreds of gigawatts of AI data center capacity using yesterday’s grid and yesterday’s power conversion architecture. The GPUs are only useful if the power chain can support them.

This matters because semiconductor economics become very attractive when a chip company moves from optional improvement to necessary infrastructure. If the customer merely wants a smaller charger, pricing power is limited. If the customer cannot build the next AI rack without solving power density, the vendor’s strategic value changes.

That is the entire Navitas 2.0 story.

The business model shift: from mobile cyclicality to infrastructure design cycles

The old Navitas was exposed to a market with short visibility and increasing price pressure. Mobile customers can behave like consumer electronics customers: short lead times, aggressive pricing, rapid iteration, and limited loyalty once the product becomes commoditized.

The new Navitas wants to serve a very different customer set: hyperscalers, power supply companies, data center infrastructure players, grid equipment manufacturers, and high-power industrial customers.

That changes the quality of revenue.

Mobile gave the company perhaps a few weeks of visibility. High-power infrastructure markets can provide longer design cycles, deeper qualification processes, and more predictable ramps once a design win is secured. That does not remove execution risk, but it does change the economic profile.

This is why the companys decision to exit mobile quickly matters. It is not merely a portfolio cleanup. It is an attempt to reallocate scarce engineering resources toward the markets where technical differentiation still matters.

For a small semiconductor company, engineering focus is capital allocation. Every engineering hour spent defending a commoditizing mobile product is an hour not spent trying to win the next AI power architecture.

That is the right strategic pivot.

The revenue lever: content per rack, not just unit volume

The most important concept is the idea that semiconductor content does not scale linearly with power.

As AI racks move from lower power levels toward much higher density configurations, the powr conversion problem becomes exponentially harder. You cannot simply add more traditional power supplies indefinitely. Space, heat, efficiency loss, and conversion complexity become binding constraints.

That creates a content-per-system opportunity.

The company is essentially arguing that as rack power increases, the amount of GaN and SiC content required per system can rise sharply. This is the critical revenue multiplier. The upside is not just more AI racks. The upside is more semiconductor content per rack.

That is exactly the kind of setup innovation investors should look for: a market where the end-demand driver is already visible, but the content opportunity is still underappreciated.

With Navitas, the bet is not simply “AI data centers will grow.” Everyone knows that. The sharper thesis is:

AI racks are becoming so power-dense that the power architecture must change, and that architectural change increases Navitas’ revenue opportunity per rack.

That is the needle-mover.

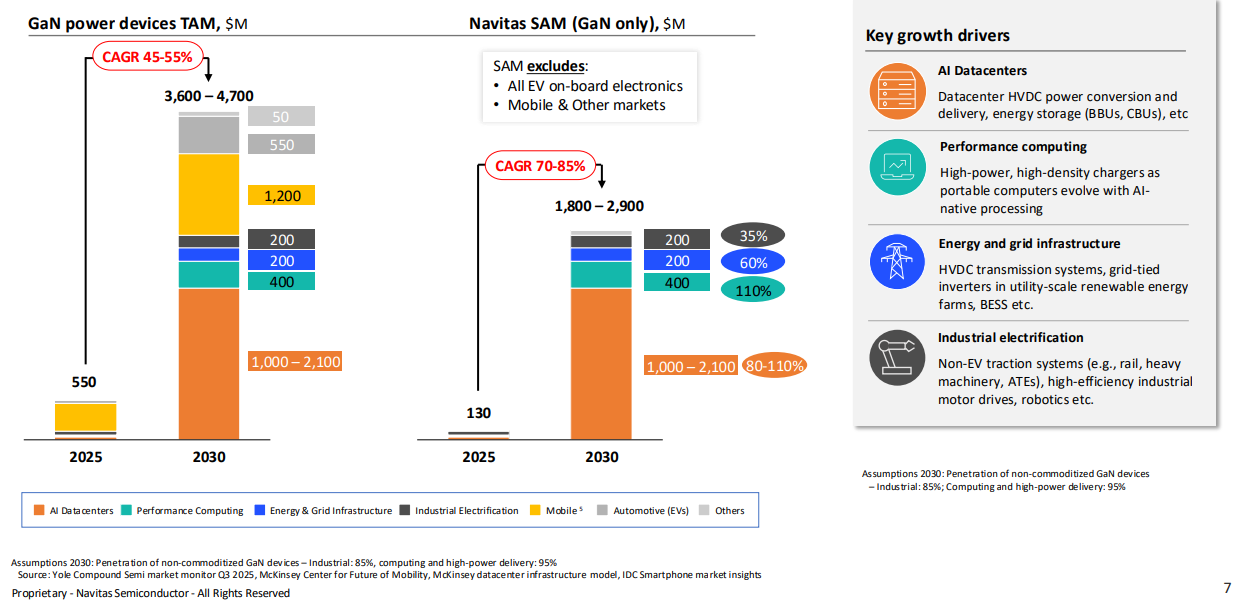

800V HVDC: the architectural inflection point

The 800V HVDC transition is the most important specific catalyst.

Today’s data center power systems involve multiple conversion steps. Each conversion loses energy, creates heat, and consumes space. As rack density increases, those losses become unacceptable. Moving toward higher-voltage DC distribution can reduce conversion losses and improve efficiency.

For Navitas, this matters because 800V HVDC is a GaN opportunity.

This is where the company’s technology history becomes relevant. Navitas is not claiming it will invent GaN tomorrow. It has spent years working with GaN, initially in mobile, and is now trying to apply that experience to higher power applications. That historical learning curve matters because power semiconductors are not simple plug and-play components. Customers need reliability, thermal performance, qualification data, system-level support, and confidence that the device will work under extreme conditions.

This is also why the company talks about boards and reference designs. Navitas is not just trying to sell parts. It is trying to help customers implement new power architectures. That is strategically important because system-level enablement can create stickier relationships and higher value capture.

The market should watch for evidence that this is moving from demonstration to commercial adoption. The key proof will not be pipeline language. It will be orders, backlog, revenue ramps, and customer validation.

The CEO was right on this point: revenue is the source of truth.

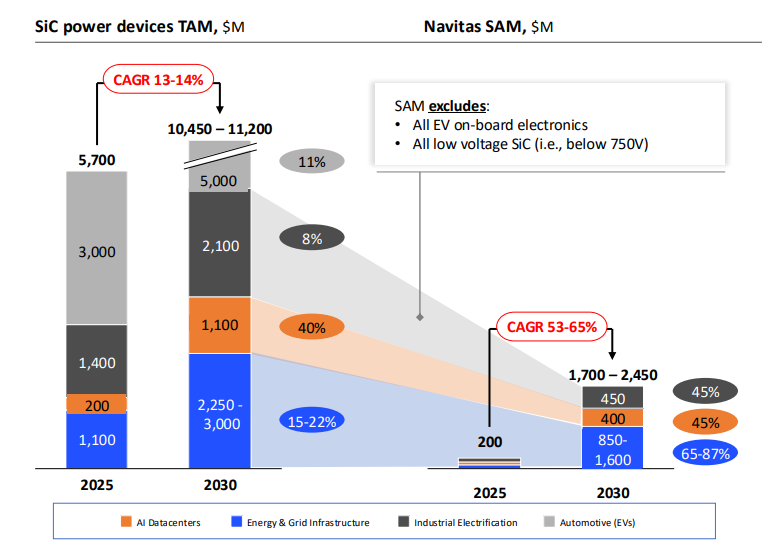

SiC gives Navitas a second monetization vector

The GaN story is important, but the SiC angle may be just as important for long-term economics.

In the AI data center, GaN may be the 800V rack-level opportunity, but SiC plays in higher-voltage conversion, power supplies, and grid infrastructure. That gives Navitas exposure both inside and outside the data center.

This dual exposure is strategically valuable.

Some competitors are more religious about one technology. Navitas is positioning itself as technology neutral between GaN and SiC, depending on what the customer needs. In high-power infrastructure markets, that may matter because customers want the right device for the right voltage, power density, reliability profile, and architecture.

The grid opportunity is also longer-duration than the data center opportunity. AI data centers may drive a five-to-ten-year infrastructure boom, but grid modernization is a multi-decade process. If AI becomes the forcing function that finally accelerates grid upgrades, SiC could give Navitas a much longer tail than investors usually associate with small semiconductor companies.

This is the second layer of the thesis:

GaN is the AI rack architecture bet; SiC is the grid and high-voltage infrastructure bet.

If both develop, Navitas is not just levered to one product cycle. It is levered to a broader electrification transition forced by AI power demand.

The margin story: mix, scale, scarcity, and system value

The margin expansion case is straightforward, but it needs to be understood through semiconductor economics.

First, mix should improve as mobile declines. Mobile is commoditizing. AI, grid, and industrial high power applications are more demanding, more differentiated, and more reliability sensitive. That usually supports better gross margins.

Second, scale matters. Semiconductor companies have fixed engineering, qualification, and suport costs. If revenue ramps while operating expenses are controlled, the incremental margin can be powerful. Navitas is still in the transition phase, but the model becomes much more attractive if high-power revenue starts scaling faster than expenses.

Third, scarcity matters. In a bottleneck economy, customers pay for the thing that enables the system to move forward. If power density becomes a binding constraint for AI infrastructure, the best power semiconductor solutions can gain pricing power, especially early in the adoption curve.

Fourth, system-level selling can improve economics. A company selling only discrete components is easier to price down. A company helping customers solve architecture-level problems can capture more value, even if the final product is still a semiconductor device.

This is why the reference board work matters. If Navitas helps define how customers move to 800V architectures, it becomes more than a parts supplier. It becomes part of the design path.

That is where margins can surprise.

The GlobalFoundries partnership is strategically important

The move from TSMC toward GlobalFoundries for GaN production is not just a manufacturing footnote. It fits the entire Navitas 2.0 thesis.

AI infrastructure and grid infrastructure are increasingly strategic markets. Customers care about supply security, geographic resilience, and domestic manufacturing. A U.S.-based foundry relationship can matter when selling into hyperscalers, grid players, and national-security-sensitive infrastructure.

This does not automatically guarantee better margins, but it can improve strategic relevance.

For a small company trying to win against larger incumbents, credibility matters. A robust, scalable, U.S.-aligned manufacturing partner could help reduce customer concerns around supply chain risk.

The risk, of course, is execution. Foundry transitions are not trivial. Sampling, qualification, yield, reliability, and production ramp all need to work. Investors should treat the GF transition as both a potential advantage and a key execution checkpoint.

Why the stock is still an option, not a proven compounder

The bull case is attractive, but the company still needs to prove it.

The biggest risk is not end-market demand. AI power demand is real. Grid pressure is real. Electrification is real. The risk is whether Navitas wins enough sockets to monetize that demand.

The CEO himself acknowledged that there are many suppliers trying to serve the AI power ecosystem. Large competitors have scale, customer relationships, manufacturing depth, and balance sheet strength. Infineon, STMicro, Onsemi, Texas Instruments, Monolithic Power, and others are not going to ignore this opportunity.

So the investment question is not, “Will the AI power market grow?”

It is:

Can Navitas convert early technical relevance into design wins, production revenue, and sustainable gross margin expansion before larger competitors absorb the opportunity?

That is the real underwriting question.

This is why Navitas belongs in the “innovation optionality” bucket rather than the “proven infrastructure compounder” bucket. The upside can be large because the company is small relative to the opportunity. But the risk is also high because the market is early, competitive, and execution-heavy.

What would make me more bullish

There are several signals that would materially strengthen the thesis.

The first is sequential revenue growth driven by high-power markets, not mobile stabilization. The company has said it expects to grow quarter over quarter through 2026. That needs to happen.

The second is gross margin improvement. If the mix shift is real, investors should eventually see it in margins. The company does not need perfect margins immediately, but the direction matters.

The third is customer validation around 800V HVDC. Not vague “engagements” but evidence of design progress, qualification, orders, or revenue contribution.

The fourth is proof that the GF transition is on track. Samples, qualification milestones, and production readiness will matter.

The fifth is backlog quality. Longer visibility is one of the major advantages of moving away from mobile. Investors should watch whether that shows up in stronger revenue predictability.

What would make me more cautious

The warning signs are also clear.

If mobile declines faster than high power revenue ramps, the transition could create an air pocket. If gross margins fail to improve despite the mix shift, the pricing power thesis weakens. If 800V adoption is delayed, the GaN data center opportunity may take longer than bulls expect. If larger competitors win the key sockets, Navitas may remain a niche player despite being directionally right.

The other risk is narrative inflation. “AI power bottleneck” is a powerful story, and powerful stories can cause stocks to price in success before the financials confirm it. For this kind of name, the discipline is to separate strategic relevance from actual monetization.

The company can be right about the market and still fail to capture enough economics.

Portfolio framing: why this belongs in an innovation basket

For an innovation-oriented equities portfolio, Navitas is not the anchor position. It is not the Nvidia of power. It is not yet the ASML of GaN. It is not a monopoly choke point.

It is better understood as a convex infrastructure option.

The company sits at the intersection of several powerful themes:

- AI data center power density

- 800V DC architecture

- grid modernization

- high-voltage SiC adoption

- industrial electrification

- U.S.-aligned semiconductor supply chains

That combination creates asymmetric upside if the company executes.

The stock should be sized accordingly. This is not a low-risk compounder. It is a “fastest horse” candidate in a very specific bottleneck: power delivery for AI-era infrastructure.

The market tends to first price the obvious AI winners. Then it prices the enablers. Then it prices the hidden constraints. Navitas is trying to become one of those hidden constraint names.

Conclusion

Navitas is attempting one of the most important transitions a semiconductor company can make: moving from a commoditizing consumer market into a structural infrastructure bottleneck. The company’s future will be driven by whether AI data centers and grid infrastructure require a new high-efficiency power architecture, and whether Navitas can convert its GaN and high-voltage SiC capabilities into real design wins. The top-line opportunity comes from rising power density, higher semiconductor content per rack, 800V HVDC adoption, and grid modernization. The margin opportunity comes from mix shift, scale, system-level value, and scarcity economics. The risk is that the opportunity is real but captured by larger players. But if Navitas executes, this is no longer a mobile charger company. It becomes a leveraged bet on the power bottleneck of the AI economy.

Leave a comment