Maybe a more suitable title could have been: “Does trend-following being profitable makes sense?”

Many traders don’t care about the reasons why they achieve profitable strategies out of trend-following techniques. They don’t want to know. For them, it suffices to keep making money out of them. For me that doesn’t work, I need to understand the underlying logic, or else I’ll lack the conviction to keep invested.

For many years, technical analysis was something I abhorred. And in some sense, I still do, but now I understand why it works most of the time. The idea that looking at a chart of past prices might tell you anything about the future made no sense to me. But, seeing it work for long periods made me uneasy about investing. How was it possible that something so silly could work, while my research on fundamentals took so long to yield meaningful results?

It was when I read the book “The Alchemy of Finance” by George Soros that it hit me. His theory of reflexivity of social sciences does a pretty good job explaining it. Basically, since we are at the same time observers and participants, our own actions influence the outcomes. Therefore, it shouldn’t be a surprise that when stocks are rising, they build momentum and they are likely to keep rising. The attention drawn to a rising stock market is self-feeding and attracts even more participants. It is incredibly simple, but it is also tremendously overlooked by many investors.

Another reflexivity issue has to do with the design of the financial system. The use of debt ratios, for instance, is tremendously misleading during euphorias. For instance, the wealth effect from a rising stock market increases the credit against those assets. The problem is that a sudden bust in asset values leaves everyone with low collateral against their debts. The following deleveraging is slow and painful.

This type of financial setup also evidences the human fallibility theory. In essence, every human construction is flawed. That means there are unintended consequences from human constructions. The rapid wealth creation originated in the exchanges tends to promote credit creation, which in turn facilitates credit crunches.

Therefore, I am no longer surprised when I see trend-following – or as they are presently called, momentum strategies – working. I have also built some momentum into my portfolios. Obviously, I don’t use technical indicators, but I do like to invest in companies that are going up while having great business models. These two factors together tend to work better than just buying an uptrend. Nevertheless, I limit those strategies to less than 20% in any portfolio, because the truth is those strategies do not work all the time, and when they’re not working, the damage tends to be big.

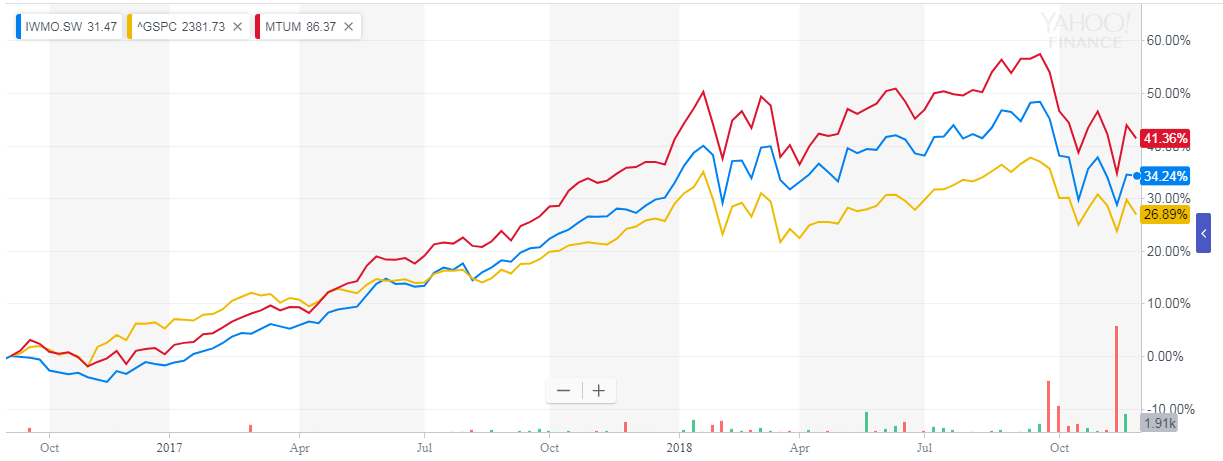

A great way to include the momentum factor in a portfolio is to buy an ETF like MTUM.

Graph 1 – IWM and MTUM ETFs performance vs the S&P 500

(Source: finance.yahoo.com)

During the last couple of years, momentum has attracted the focus of the investor community. Therefore, several ETFs trying to capture that factor have appeared on stage. In recent years it has beaten the S&P. However, I think what really happened was that momentum has, in fact, exacerbated the S&P performance. Meaning that when a really bad downturn comes our way, it will be felt accordingly.

The best advice I can give is to understand the assumptions built into the uptrend, and if they are starting to look unsustainable, just fold. Don’t stay in the game just because everyone seems to be making loads of money. Remember lots of intelligent people, like Isaac Newton, made this mistake. In the late stages of a trend, reflexivity and human fallibility make the momentum seem invincible. That’s when you run.

(Photo credit: Wagner T. Cassimiro)

If you liked, please subscribe. We won’t spam you.

Leave a comment