Nebius’ (NBIS) Q1 2026 earnings were not just strong. They were a signal that the company is moving from AI infrastructure promise to AI infrastructure execution.

Source: Author

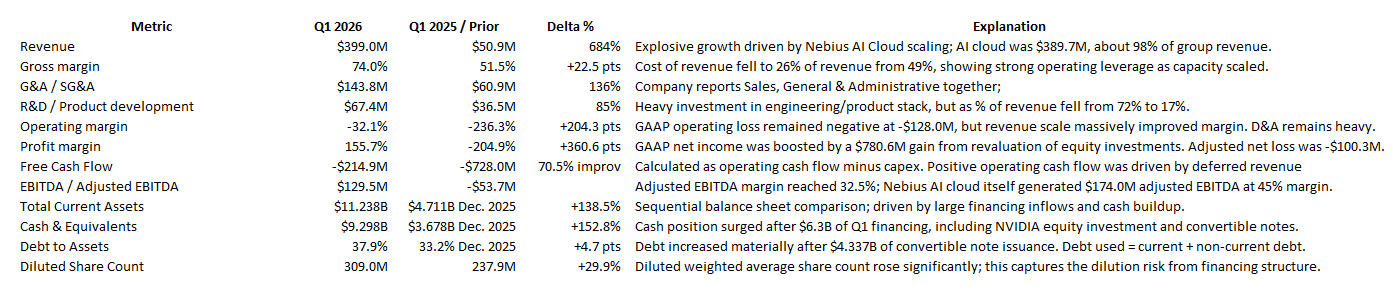

Revenue grew 684% year over year to $399 million, while Nebius AI Cloud revenue reached $389.7 million, up 841% year over year. The AI cloud business now represents roughly 98% of group revenue, which means the investment case has become much cleaner: Nebius is now primarily an AI cloud and AI factory company.

The stock remains high risk because this is a capital-intensive bildout. But the important development is that dilution and capex are now being matched by real customer demand, real operating leverage, and strategic validation from Meta and NVIDIA.

My thesis is simple: Nebius is one of the cleanest public market bets on the industrialization of AI compute.

Nebius Is No Longer Just A Story Stock

There are moments in a company’s life when the narrative either collapses under the weight of execution, or execution finally catches up with the narrative. Nebius just had one of those quarters. For much of the past year, the debate around Nebius was simple: is this another AI infrastructure hype vehicle, or is this one of the few companies actually positioned to build the physical layer of the AI economy?

Q1 2026 pushed the answer closer to the second camp. Group revenue reached $399 million, up from $50.9 million a year ago. Adjusted EBITDA moved from a $53.7 million loss last year to $129.5 million positive this quarter. Cash and equivalents ended the quarter at $9.3 billion. That is not a minor inflection. It tells us that Nebius is not just raising capital into an AI dream. It is turning capacity into revenue, revenue into operating leverage, and strategic partnerships into financing power.

Nebius is no longer being valued only on what it might build. The market now has numbers showing what happens when the AI factory turns on.

The Real Business: Monetizing The Compute Shortage

The first and most important thing to understand about Nebius is that it is a bottleneck economy company. In the old software world, the bottleneck was distribution. In the AI world, the bottleneck is increasingly physical: GPUs, power, data centers, networking, cooling, deployment speed, and inference efficiency. Nebius sits directly inside that constraint.

The company’s Q1 shareholder letter says demand remains far above available capacity, with customers moving beyond experimentation into realworld AI applications. AI compute is moving into healthcare, robotics, enterprise workflows, model builders, support automation, and physical AI. That matters because Nebius is not trying to be a generic cloud provider. It is trying to become a fullstack AI production platform.

It sells compute, but the bigger ambition is to own the factory floor of AI. The first AI wave was about building models. The next wave is about running them everywhere. We need the cloud that makes that possible.

Earnings Show The Flywheel Is Starting To Work

The earnings report gives us three signals that matter. First, revenue is scaling at extraordinary speed. Group revenue grew 684% year over year, while AI cloud revenue grew 841% year over year. ARR reached $1.92 billion, up 674% year over year and 54% sequentially. Second, operating leverage is appearing. Cost of revenue fell from 49% of revenue to 26%. Product development fell from 72% of revenue to 17%. SG&A fell from 120% of revenue to 36%. Third, the core AI cloud business is already showing attractive economics. Nebius AI Cloud generated $174 million of adjusted EBITDA at a 45% adjusted EBITDA margin in Q1.

That is the number that should make investors stop and think.

This is not yet a mature business. It is still investing aggressively. It is still absorbing massive depreciation and amortization. It is still in the middle of a capital untensive expansion. But at the segment level, the AI cloud business is already proving that scale can produce real margin.

We have been saying for a long time that the first GPU cluster is expensive. The next customer is where the operating leverage starts to appear.

The AI Factory Thesis

Nebius is not merely renting GPUs. That would be a weaker thesis. The better thesis is that Nebius is building AI factories. The company now has more than 3.5GW of contracted power, has raised yearend contracted power guidance to more than 4GW, and expects 800MW to 1GW of connected power by year-end. Owned capacity now represents more than 75% of contracted power.

Colocation gives speed, but owned infrastructure gives control. It can improve long-term unit economics, reduce dependence on third party data center providers, and allow Nebius to design the infrastructure around AI workloads instead of adapting generic cloud architecture to AI demand.

This is why the Pennsylvania, Missouri, Finland, Alabama, and New Jersey capacity buildouts are not just real estate announcements. They are the foundation of the future margin structure. Remember taht for all purposes, contracted power is the promise, connected power is the catalyst, and active power is the earnings engine.

Meta And NVIDIA Change The Quality Of The Story

The two most important external validators are Meta and NVIDIA. The new Meta agreement is worth up to $27 billion. It includes a $12 billion five-year purchase of compute capacity beginning in early 2027, plus an additional $15 billion structure that allows Nebius to allocate capacity either to Meta on pre agreed terms or to AI cloud customers at market rates. That structure is powerful.

It gives Nebius long-term visibility while preserving upside if market pricing remains strong. It also helps with financing. In capital-intensive infrastructure, demand visibility is not just a commercial advantage. It is a balance-sheet tool.

Then there is NVIDIA, the kingmaker, whgich invested $2 billion in Nebius and deepened the partnership across hardware, software, AI factory design, inference, and agentic AI. Nebius also achieved NVIDIA Exemplar Cloud status on GB300 NVL72 for training workloads.

This matters because NVIDIA does not need to validate every AI cloud. Its involvement tells the market that Nebius is not merely a buyer of GPUs. It is becoming part of the AI infrastructure ecosystem. Meta gives Nebius demand visibility. NVIDIA gives it ecosystem credibility.

The Next Margin Lever: Inference Optimization

The market still talks about AI infrastructure as if it is only about GPUs. That is too simplistic. The next layer of differentiation will be efficiency: how many tokens can you generate per GPU, per watt, per rack, per dollar? That is why the acquisitions of Tavily, Eigen AI, and Clarifai matter. They move Nebius up the stack from infrastructure into retrieval, agentic workflows, inference execution, model optimization, and system level orchestration.

Eigen AI strengthens Nebius Token Factory as a managed inference platform. Clarifai adds system level inference optimization and engineering talent. Tavily adds agentic search capabilities. This is the strategic direction investors should focus on.

If Nebius remains just a GPU landlord, the business will eventually be judged on commodity infrastructure economics. But if Nebius can become a production platform for inference and agentic AI, the company can improve utilization, increase customer stickiness, and expand revenue per GPU. In the end, the bull case is more revenue from every GPU.

The Financial Picture: Stronger, But Not Clean

The quarter was impressive, but investors should not confuse headline GAAP profitability with clean operating profitability. Nebius reported $621.2 million of net income from continuing operations, but that was heavily influenced by a $780.6 million gain from revaluation of investments in equity securities, largely tied to the increased value of its ClickHouse stake.

The cleaner operating view is adjusted EBITDA and adjusted net loss. Adjusted EBITDA was positive at $129.5 million, but adjusted net loss was still $100.3 million. This tells us the business is progressing rapidly, but still not fully through the investment phase. The margin picture is encouraging, but depreciation and amortization remain heavy because the company is buying GPUs and data center hardware at scale. D&A was $212 million in Q1, up 332% year over year. That is the nature of this business.

This is not SaaS. This is infrastructure. Investors must analyze Nebius like a hybrid of cloud provider, data center developer, GPU fleet operator, and project-finance machine.

Dilution Risk Is Real

The biggest risk is not demand today. The biggest risk is the capital structure. Nebius spent approximately $2.5 billion on capital expenditures in Q1, primarily for GPUs, GPU-related hardware, and data center expansion. The company raised $6.3 billion in Q1, including $4.3 billion of convertible notes and $2 billion from prefunded warrants linked to NVIDIA’s investment.

The diluted weighted average share count rose to approximately 309 million, compared with 237.9 million a year earlier. The company also had 253.9 million shares issued and outstanding at quarter-end, excluding treasury shares. So yes, dilution is not theoretical. It is already part of the story. But not all dilution is equal.

Bad dilution funds losses without creating durable earnings power. Good dilution funds capacity that is already supported by demand, prepayments, strategic customers, and high utilization. For now, Nebius’ dilution looks more productive than destructive because revenue is scaling, adjusted EBITDA has inflected, and strategic contracts are improving revenue visibility.

But this must be monitored carefully. Nebius is racing two clocks: the AI capacity clock and the dilution clock.

Risks

The first risk is execution. Nebius must bring large-scale AI factories online on time and within reasonable cost. Delays in power, data center construction, GPU supply, networking, or customer deployment would hurt the thesis. The second risk is financing. The company will likely need more capital. If equity issuance, converts, warrants, or SBC grow faster than operating value, shareholders can be diluted even if revenue grows. The third risk is pricing. AI compute is scarce today, but supply can eventually catch up. If GPU rental pricing compresses before Nebius fully monetizes its capacity, margins could disappoint.

The fourth risk is technology cycles. AI infrastructure depreciates quickly. If new GPU generations make older fleets less attractive faster than expected, Nebius may need to reinvest aggressively to stay competitive. The fifth risk is customer concentration. Large strategic deals are useful, but dependence on a few major buyers can create negotiating pressure over time. The sixth risk is accounting noise. GAAP net income benefited from investment revaluation gains this quarter, so investors should focus on operating metrics, adjusted EBITDA, free cash flow, capex, and diluted share count.

Final Thesis

Nebius is becoming one of the clearest public-market expressions of the AI infrastructure bottleneck. The company is securing power, building AI factories, deploying GPU capacity, signing strategic customers, moving up the stack into inference, and showing early operating leverage. The quarter matters because it gives the thesis proof.

Revenue is exploding. AI Cloud margins are already strong. Meta and NVIDIA are validating the platform. Owned capacity is growing. The software layer is deepening. The balance sheet has been reinforced.

But the stock is not without risk. This is a capital-intensive buildout, and investors must watch dilution as closely as growth. My view: Nebius is increasingly credible AI infrastructure compounder. The stock works if Nebius can turn power into active capacity, active capacity into revenue, and revenue into per-share economics faster than dilution eats the upside. Nebius is not just selling compute. It is industrializing compute.

Leave a comment