There is a simple reason I remain constructive on IREN: the company no longer looks like a pure “AI demand is big” story, it is increasingly a story about whether scarce, energized, deployable infrastructure can command better economics in a market that still cannot clear.

The bullish case for IREN has evolved. The original thesis was mostly about power scarcity, land, and the companys ability to convert those physical assets into AI infrastructure. That was the credibility phase. The market wanted proof that IREN had real assets, real counterparties, and a plausible path from mining-adjacent infrastructure to AI cloud monetization.

Now the debate is changing. The market is beginning to ask “can IREN convert that infrastructure into better economics as scarcity persists across the stack?” I think the answer is increasingly yes, and the recent breadcrumbs around pricing power are the reason.

The Important Shift: Scarcity Is Not Just About The Newest GPU

A few recent datapoints, widely circulated in investor and industry channels, point in the same direction.

First, there were reports that rental pricing for older-generation NVIDIA H100 GPUs has remained firm or even increased in 2026 despite the product being several generations old.

source: x.com

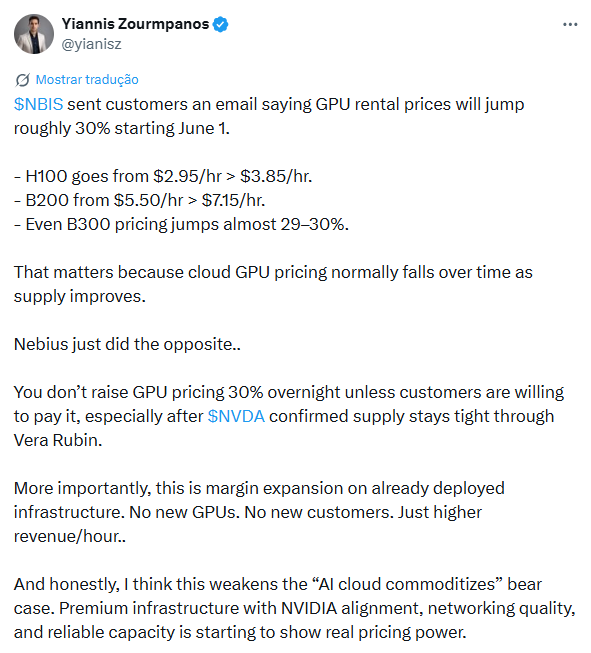

Second, there were reports that Nebius raised on-demand pricing materially while a third-party availability index for cloud GPU supply dropped sharply. If those datapoints are directionally correct, the message is powerful: AI compute scarcity is broader than just the newest chip launch cycle.

source: x.com

If older-generation GPUs are still commanding better-than-expected pricing, and if cloud availability is falling even as prices rise, then the bottleneck is no longer just about headline silicon supply. It is about deployed, usable, ready-to-run compute. That should be top of mind to anyone analyzing IREN.

Because customers are not really buying chips in the abstract. They are buying time-to-compute, and in a constrained market, the premium goes to whoever can make compute available now, not whoever tells the prettiest story about theoretical future capacity.

Why This Matters More For IREN Than It First Appears

For some AI infrastructure peers, tight on-demand pricing has an obvious read-through. Operators with meaningful merchant exposure can potentially feel the benefit more quickly in current pricing, utilization, and near-term cloud economics. IREN is different.

The more important implication for IREN is not that all existing contracts immediately reprice upward. They likely do not. The significance is that future negotiations may take place in a tighter market than the one in which the company signed its earliest anchor arrangements.

The first Microsoft deal was valuable because it established credibility. It told the market that IREN was not just a speculative infrastructure owner but a real participant with bankable counterparties. The criticism, of course, was that the economics looked underwhelming relative to the enthusiasm around the stock.

I think that critique partly misses the sequencing. The first deal did not need to be the peak of economics. It needed to be the entry ticket. Once credibility is established, later capacity can be negotiated in a market that now appears to be tighter, more supply-constrained, and more aware that time-to-compute carries real value. In that environment, the next tranche of capacity does not have to clear on the same terms as the first one.

That is the pricing-power trade.

Pricing Power In Infrastructure Does Not Always Show Up As A Sticker Price Increase

One of the mistakes investors make in this space is looking for pricing power only in obvious headline form. They expect to see a clean statement that says: rates went up.

That is not usually how it works in infrastructure.

Pricing power can show up in quieter ways:

- better revenue density per megawatt

- stronger monetization of already-built halls

- faster fill rates for energized capacity

- improved counterparty quality

- better prepayments or financing support

- higher returns on sunk infrastructure

If the company is able to monetize premium Blackwell demand into existing or largely prepared infrastructure, the economics can improve even if the deal looks small in megawatt terms. The reason is straightforward: when the shell, power, team, and much of the fixed cost base are already in place, the incremental return on monetized capacity can rise meaningfully.

That is a subtler and more important form of pricing power than simply charging a visibly higher hourly rate.

The Market Signal From Scarcity: Availability Collapsing While Prices Rise

The most important recent signal, in my view, is the combination of two things happening at once:

- on-demand pricing reportedly moving higher, and

- reported cloud GPU availability deteriorating materially

That combination matters because it suggests the market is not clearing. In other words, higher prices are not yet enough to balance supply and demand.

That is exactly the environment in which real infrastructure owners gain leverage.

And I do not mean “owners” in a generic sense. I mean operators that actually have the ingredients that matter in this cycle:

- secured power

- data center development capability

- GPU deployment experience

- energized or near-energized facilities

- the ability to turn capacity into live compute

That is why I believe the scarcity signal is more important for IREN than many investors realize. It raises the value not only of contracted capacity, but also of any retained or not-yet-contracted capacity that can be brought to market with certainty.

The Main Risk: Scarcity Without Execution Is Just Expensive Optionality

The bullish argument is improving, but the risks remain real. The biggest one is that pricing power remains more inferred than proven. The breadcrumbs are encouraging, but investors still need to see the economics show up in the facts:

- better contract structures

- stronger monetization per MW

- disciplined capital deployment

- visible AI revenue conversion

- evidence that newer tranches earn better returns than earlier ones

There is also the risk that supply eventually catches up, or that efficiency gains in model architecture reduce the scarcity premium faster than expected. I do not think that is the most likely near-term outcome, but it cannot be ignored.

Finally, IREN is still a capital-intensive build story. Even strong financing terms and strategic alignment do not remove the basic burden of proof. The company now needs to show that cheap capital can be turned into high-return assets rather than simply a larger asset base.

Leave a comment