Summary

- A couple of weeks ago, I proposed that the virus would make an impact on the economy, and, by default, on the complacent market.

- Now, it seems like the virus is spreading out of China, and the biggest world economies are activating the debate around stimulus.

- Big organizations will likely get access to the stimulus, but it is critical to understand how smaller companies will cope with this crisis.

Photo Credit: susanjanegolding

A few weeks ago, I wrote about the coronavirus threat to the world economy and the markets. In that text, I said that the economic impact of the current virus would be higher than the SARS iteration. Now, I’m no virus expert. However, even in the early days, it was clear to me that the virus was much more contagious than the SARS, which, given the higher interconnectedness between China and the rest of the world, meant that the spread could get scary.

After the initial outbreak, China provided a strong and determined response. The country acted swiftly and decisively to contain the virus, even at the expense of air travel, tourism, and industrial production. In my non-expert opinion, that’s the price to pay to try to control the virus threat.

However, parallel to that, there is a huge side effect on the financial sector. Finance runs on time. For instance, interests are due periodically, we use day count conventions to be precise on the interest expense, bills are due in X number of days, and investors expect periodical reports from publicly traded companies, among others. The problem here is that the measures to control the virus are making the world economy to slow down, while its financial mirror has no inherent mechanism to reflect that.

All that seems like a dangerous setup, which might be the catalyst for financial panic. Companies, like Apple (NASDAQ:AAPL), are already feeling the impact of lower demand and lower production output. Now, you might argue that Apple is more than capable of withstanding the shock, and you’re probably right. On that line of thought, a stimulus is also on the way for big financial companies. We should be fine, right? Not so fast. I am focusing on the impact on small-and-medium enterprises, especially the ones with outstanding bank loans.

These companies won’t get most of the monetary stimuli and will have debt payments due, without enough cash flow to cover them. Banks will demand payments on time and won’t hesitate to call for bankruptcy, in case companies don’t pay. This might very well trigger a wave of defaults within the small and medium enterprises, which might kick yet another problem for big financial companies.

Working hypothesis

My first hypothesis was that the higher contagiousness of the virus would make a far more serious problem than was the SARS. Now, I am updating my testing hypothesis. First, I am comparing the spread of the disease in South Korea and Italy to the outbreak early in January in China, and second, I am focusing on its impact on the broad economy, starting from the SMEs as the reference.

H0.1: Italy and South Korea will mimic the same pattern that followed the outbreak in China back in January. Other countries will follow the same process.

H0.2: The financial system is not prepared to accompany the slowdown of the economy and commerce, and it will automatically generate a de facto monetary tightening.

If these two hypotheses materialize, we will see serious troubles in the markets and the economy. Investors will oversell risk assets and overbuy safe-haven assets. Honestly, we shouldn’t let emotions get the better of us. Investors must be reasonable and calm throughout uncertainty and though times. However, at this stage, it seems like not enough market participants recognize that this virus might be the catalyst to financial turmoil on a scale we have not seen since the 2007 financial crisis.

So far, H0.1 seems to be materializing with the number of cases exploding in both countries.

Source: Worldometers

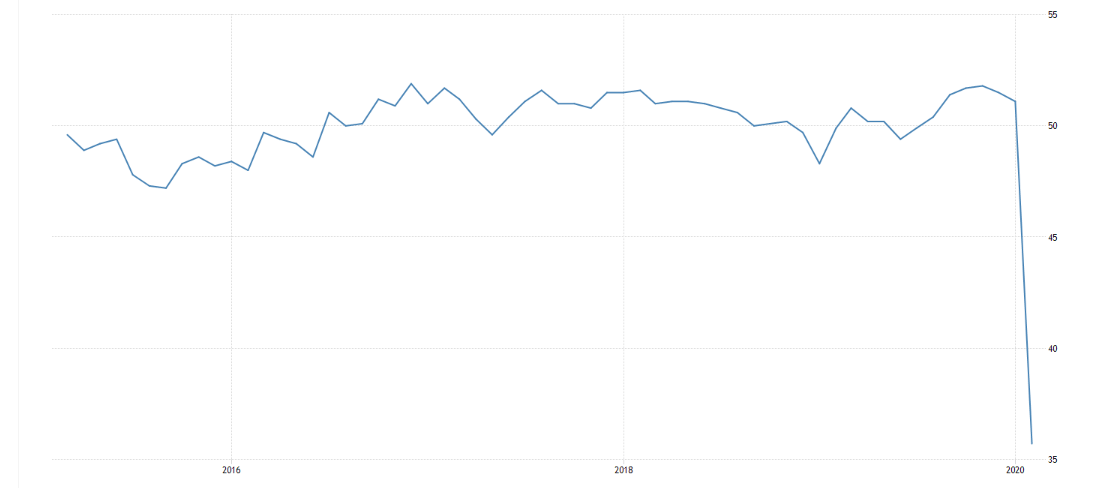

On H0.2, Chinese PMIs are out, and they don’t look good.

Source: Trading Economics

Final Remarks

The jury is still out on how the financial system will cope with the violent slowdown in economic activity. If the slowdown doesn’t ignite a series of bankruptcies in SMEs, then I believe that investors might retain its confidence in the solidity of the financial system. However, if the financial system is unable to cope with these extraordinary circumstances, things might turn sour very fast.

In my opinion, the fact that there is little visibility about mechanisms for the SMEs to cushion the crisis means that, probably, there is no concrete plan. Likely, we will start to see companies struggling a long time before bureaucrats come up with some plan to avoid disaster.

That will lead to further bad economic readings. Possibly, we might get some upticks in the unemployment rate, which could foster distrust among market participants. Or maybe I am just overthinking.

Be as it may, the market will, likely, remain sensitive to the current crisis. At least, until it identifies a credible way out, which might be a vaccine or simply warmer weather kicking the virus out.

Disclosure: I am/we are long GLD. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: This text expresses the views of the author as of the date indicated and such views are subject to change without notice. The author has no duty or obligation to update the information contained herein. Further, wherever there is the potential for profit there is also the possibility of loss. Additionally, the present article is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Some information and data contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. The author trusts that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.

Leave a comment