Photo credit: Fritzchens Fritz

The narrative

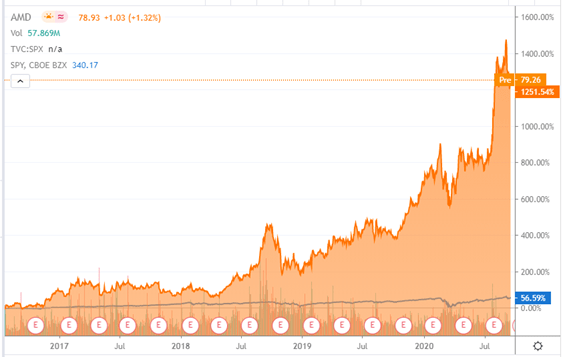

Advanced Micro Devices (AMD) has been a star stock for the last couple of years. In the same period that the S&P 500 rose 56%, AMD put on an impressive 1251% run. Basically, AMD mixes a turnaround story with a growth narrative.

(Source: Seeking Alpha)

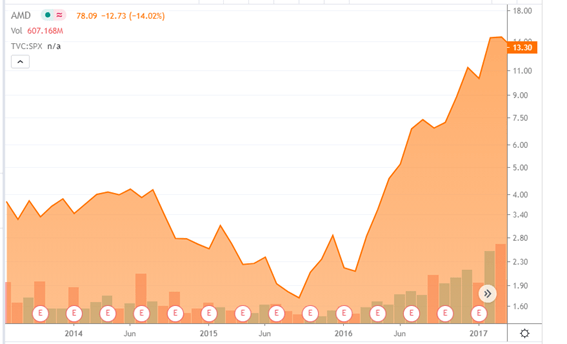

The company has been a wild ride since its inception. Periodically, investors flocked to this stock in hope, only to leave it, later on, amid fears of execution struggling. AMD remained on Intel’s shadow, as it became evident that the scale advantages were huge and in Intel’s favor.

(Source: Seeking Alpha)

The company had been working on a turnaround for a couple of years, at least since appointing Lisa Su as CEO (here is a good analysis on those efforts). The breakthrough came in 2016. A competitive product lineup brought hope of regaining market share, and by the end of the year a deal with Alibaba for processing capacity in datacenters was a perfect example of the successful recovery. The stock price followed the developments.

(Source: Seeking Alpha)

A couple of tailwinds helped from 2016 onwards. The blockchain fever, the growth in datacenters usage, and now, the work-at-home expansion have been very positive for the company. However, the main drivers for change seemed to be a redefinition of the roadmap, better product design, a huge improvement in execution, and more focus on the corporate market. Those things together seemed to be the main catalyst, while the tailwinds just gave it more visibility among the investment community.

One interesting sign was the way AMD reorganized. The company was known for having great engineers, but also for being lousy at execution. The company brought in Jim Keller in 2012. Jim is considered a fixer in chip operations, and it seemed like he was a key player in turning a company known to be lousy at execution into a serious competitor. That shows how serious the company was at reorganizing its structure, recognizing how flawed it was.

The numbers

Given the narrative we’ve just laid, let’s reconcile it with the numbers. I believe that benchmarking could offer a better perspective on the whole picture. Therefore, let’s use Intel (INTC) and Nvidia (NVDA) as a comparison. Note that we are not interested in absolute figures. For instance, accounting differences between companies make it hard to compare margins. What we can compare is the evolution of those numbers. Looking at the evolution of gross margins during the last five years, we can see that Intel’s gross margin has slowly declined. Nvidia, on the other hand, is steadily improving its gross margin. The same happens with AMD, but in this case, the improvement is huge.

(Source: Author’s computations based on 10-Ks)

Growing revenues helped to improve AMD’s performance, basically, a higher scale resulted in more efficiency. The same goes for Nvidia. In Intel’s case, revenues grew, but that didn’t translate into better gross margins, which adds to the narrative of the company losing its edge, and suffering from the competition. As we will see later, some classic corporate moves allowed Intel to mask its woes.

(Source: Author’s computations based on 10-Ks)

If AMD’s gross margin improvements were good, the operating margin performance was even better. The company turned from -12% operating losses to 9% operating profits in five years. Nvidia posted a great performance, while Intel, interestingly, also improved its operating margin.

(Source: Author’s computations based on 10-Ks)

It is a very interesting exercise to dissect how the companies improved the operating margin. AMD increased its SG&A and R&D absolute figures by 55,6% and 63,4%, respectively. However, these items as a percentage of sales actually declined slightly during the period. The pattern was similar for Nvidia. On the other hand, Intel slashed its absolute SG&A costs by 22,4%, while its R&D costs only grew by 10%. As a percentage of revenues both items were significantly reduced. Basically, Intel retorted to lay-offs and other similar measures to mask the decline of gross margins.

Finally, a huge boon for Intel and NVidia was the tax cut promoted by the current Administration. AMD was coming from a couple of years of losses and, therefore, its tax bill has only increased. However, the tax rate is low for every one of these companies, which makes me wonder if they won’t become the target of a future Administration that wants to target low corporate tax rates.

(Source: Author’s computations based on 10-Ks)

There are other indicators that AMD is on the right track. Companies in a clear path to improvement tend to clean their balance sheet from years of excessive borrowing. AMD did just that. The debt-to-assets ratio declined from 43% in 2016 to 8% in 2019. The company is now in a much better position to face adverse scenarios.

Takeaways

The numbers back up AMD’s turnaround story. The growth expectation is also there, and the following years will demand even more computing power from chipmakers. Therefore, the importance of starting to select winners and losers in this sector will be critical for the performance of investment portfolios in the coming years.

However, this game is not just about selecting great companies. It is also about paying the right price for them. And in that regard, the current valuations are off-the-charts. Buying AMD or Nvidia means paying more than eighty times forward estimated GAAP earnings and more than ten times sales. These are outrageous numbers. What scares me the most is that everyone keeps telling me that this time is different because the MMT framework is supporting valuations. Nonsense.

(Source: Seeking Alpha)

Yes, the fact that we are in an era of quantitative easing does play a huge role in pushing the valuations higher. What I don’t buy is the idea that QE is something that will never go away, and because of that, I have to buy assets at an infinite price to earnings ratios. I have strong doubts that the future will unfold in a way that rewards buying at the current levels. If that’s the macro perspective, on a micro-level, the current valuations assume perfect execution, which is unrealistic. For that to happen, most future developments would have to be positive. For instance, the tax rate would have to remain unchanged, and the company would have to keep improving its technological edge, among others. That’s not going to happen. The company is likely to enter a virtuous cycle, but that doesn’t mean perfection.

That’s what brings me to this piece. I’m not buying these companies at the current valuations, but I want to understand them, in case the near-extinct bear visits us. AMD has gone through the pains of restructuring, and it is still small when compared to Intel. However, it has reorganized well, and it is starting to grow market share profitably. Unfortunately, the market has already acknowledged that, but I think that we are on a secular trend toward more computing power and new specialized processing applications that will demand even more from chipmakers. I don’t see it as a game of winner takes all. I see lots of possible new market segments, with ups and downs along the way, that will allow chipmakers to specialize and derive good profits. And, AMD is now in a good position to do just that.

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

Additional disclosure: This text expresses the views of the author as of the date indicated and such views are subject to change without notice. The author has no duty or obligation to update the information contained herein. Further, wherever there is the potential for profit there is also the possibility of loss. Additionally, the present article is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Some information and data contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. The author trusts that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.

Leave a comment