Executive Summary

Central banks and regulators have fueled debt growth, leading to potential economic instability; Bitcoin offers a hedge against risks.

Bitcoin’s predictive nature and self-custody capabilities make it an attractive investment for protection against lurking financial threats.

Grayscale Bitcoin Trust provides a related, alternative investment option for traditional investors seeking exposure to Bitcoin without having to self-custody it.

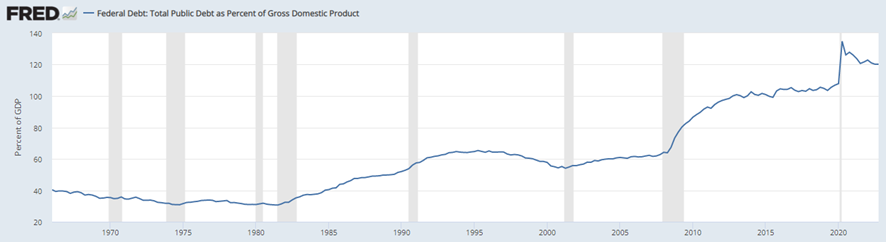

Regulators, central banks, and policymakers have committed significant blunders. In the aftermath of the 2007 crisis, they devised a framework to bolster the banking industry’s stability. These solutions were apt for the time and facilitated a decade devoid of major banking incidents. However, they overlooked one crucial trend – the persistent use of debt to propel economic growth. Consequently, debt has become increasingly pervasive, with its relative weight in the economy now more than double its pre-2007 levels.

FRED

In essence, regulators established a framework that encouraged banks to voraciously acquire treasuries. Coupled with the COVID crisis stimulus, this resulted in banks being incentivized to purchase debt at the most unfavorable prices. Presently, depositors are motivated to seek higher yields, while banks lack incentives to offer higher rates for deposits or liquidate their holdings. The majority of banks (XLF) are now effectively zombies, and the Fed’s monetary policy only exacerbates the issue.

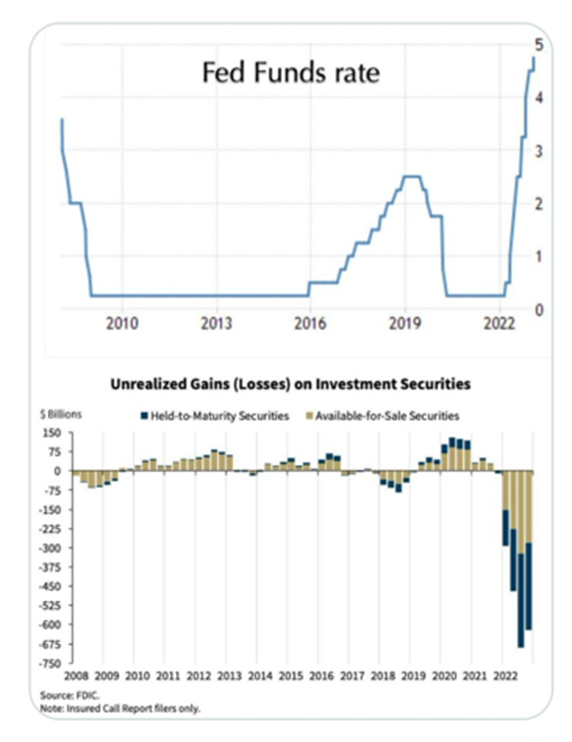

At this juncture, the Fed faces two primary options: either shatter the economy until inflation is tamed or permit debt reduction via inflation. In both scenarios, they are in a tight spot. I am convinced that they will initially attempt the former, but the ensuing damage will be so extensive that they will ultimately be left with no choice but to resort to the latter.

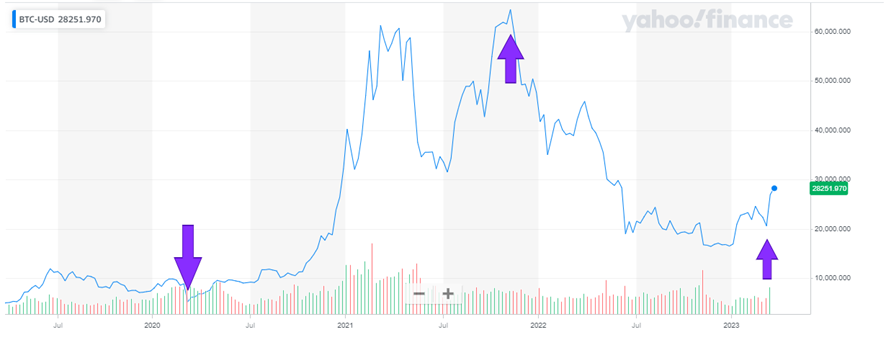

Rather than simply criticizing regulators, I’d like to offer potential solutions for investors to explore and investigate further. In my opinion, Bitcoin has proven to be a remarkable forecaster of macroeconomic trends. For example, it surged when it anticipated the massive liquidity injection into the economy in March 2020, and showed signs of weakness in the first half of 2021, which led to capitulation in the second half, clearly indicating the end of monetary indulgence. Presently, I believe Bitcoin is signaling that central banks are trapped and left with no other alternatives. The first consequence is bonds are going higher (IEF) (TLT).

Yahoo Finance

In my perspective, Bitcoin serves as an optimal safeguard against the numerous lurking risks. The most apparent of these risks is the issue of deposit guarantees. With Bitcoin, there’s no possibility of going to sleep thinking you possess a $1 million bank account only to wake up and discover you’re left with a $250k public guarantee and $750k in unsecured loans to a bank. I find it perplexing that so many people were eager to celebrate the downfall of VCs, simply because they were on the verge of losing their investments. In my view, this matter is fundamentally about private property, which lies at the core of investing.

Bitcoin addresses two primary concerns: it enables self-custody, allowing you to sidestep Uncle Sam’s influence over your property, and it is acutely sensitive to monetary expansion, helping you avoid Uncle Sam’s infamous penchant for currency devaluation. However, I recognize that this also carries numerous other risks, and many traditional investors may not be interested in acquiring the technical knowledge required to own Bitcoins directly. That’s why I propose an alternative, related asset for consideration: the Grayscale Bitcoin Trust.

When considering the Grayscale Bitcoin Trust (GBTC), it is important to acknowledge the controversy it has stirred up regarding Grayscale and DCG. Nonetheless, we should also recognize that the trust’s structure has served its intended purpose by shielding it from the sponsor and related parties, despite the fact that it is currently trading at a significant discount.

In my view, this insulation feature has helped GBTC steer clear of the worst of the DCG/Grayscale drama. Additionally, the discount it trades at is the main side-effect but could very well present a promising opportunity for investors who are willing to look beyond the noise and focus on the trust’s underlying fundamentals. Nevertheless, it is important to stress that there are differences from owning GBTC and owning BTC.

A primer on Grayscae Bitcoin Trust

The sponsor of the Trust is Grayscale Investments, LLC, which is a wholly-owned subsidiary of Digital Currency Group, Inc., commonly DCG. Grayscale Investments is responsible for the day-to-day administration of the Trust.

The formation of the Grayscale Bitcoin Trust dates back to 2013, with the purpose of holding Bitcoin. To achieve this objective, the trust periodically issues common shares to accredited investors, who provide deposits of Bitcoin in exchange. As per the most recent 10-K report, the trust currently holds around 3.3% of the total Bitcoin in circulation.

It is worth noting that the trust issues shares solely in blocks of 100 shares to specific authorized participants. In exchange for Bitcoins, these authorized participants offer baskets to the trust. This process enables the trust to maintain its holdings of Bitcoin and continue to issue shares to interested investors.

The value of a Basket of shares for the Grayscale Bitcoin Trust in U.S. dollars is established through the Index Price. This is the price of a Bitcoin, which is computed using a weighting algorithm based on price and trading volume data from selected Digital Asset Exchanges over the preceding 24-hour period.

It is important to note that the shares issued by the trust are not obligations or interests of either the Sponsor or the Trustee. Rather, they are an instrument for investors to gain exposure to Bitcoin through the trust’s holdings of the digital asset.

In theory, investing in the Grayscale Bitcoin Trust carries a low level of credit risk due to the nature of the shares. The trust’s Bitcoins are not subject to borrowing agreements with third parties. Moreover, the trust’s Bitcoins are subject to minimal counterparty and credit risk, as they are primarily held by a Custodian. This reduces the risk of loss or theft of the digital assets, which in turn minimizes any credit or counterparty risk associated with the GBTC.

The primary objective of the Grayscale Bitcoin Trust (GBTC) is to hold Bitcoins and reflect their value based on the Index Price, less the trust’s expenses.

The GBTC Trust: A Rollercoaster Ride of Drama, twists and yet more drama

The last quarter of 2021 witnessed a sharp decline in digital asset prices, which in turn caused a market-wide drop in trading prices and liquidity. This development led to financial hardships for various industry participants, causing concern and uncertainty.

The first half of 2022 saw a further deterioration of the digital asset market, leading to prominent industry participants such as Celsius Network LLC, Voyager Digital Ltd., and digital asset hedge fund Three Arrows Capital declaring bankruptcy. These events dealt a blow to the confidence of investors and further eroded the industry’s overall stability.

Later in November 2022, FTX, which was the third largest digital asset exchange in terms of volume, ceased customer withdrawals, sparking rumors of potential liquidity issues and possible insolvency. These events have further contributed to the overall instability of the digital asset market. The situation was exacerbated by the bankruptcy filings of other entities such as BlockFi Inc. and Genesis, which were impacted by FTX’s bankruptcy filing.

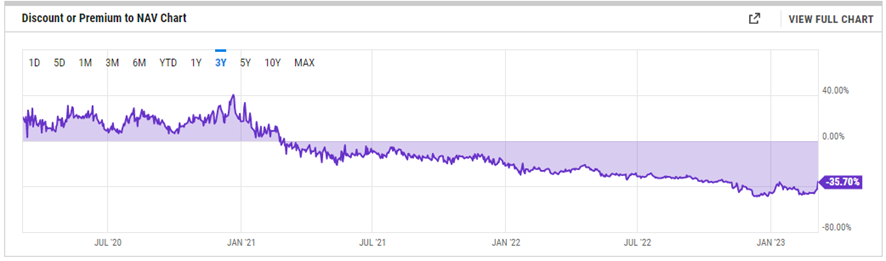

The trust has traded at premium in past, mainly due to lots of institutionals trying to enter the space and arbitrage trades. More recently, with the crypto downturn and FTX debacle, the fund turned to a steep discount.

YCharts

If you thought the situation was already suspenseful, let me tell you, it gets even better. DCG put up its GBTC holdings as collateral to grab a $575 million loan from its subsidiary Genesis. And then, DCG went ahead and invested $778 million in GBTC shares from March 2021 to June 2022 with the expectation that the net asset value discount would close.

Genesis was also lending to the Three Arrows Capital (3AC) for the same purposes. After 3AC implosion, in June 2022, it exposed Genesis to insolvency and contributed to the NAV decline in a reflexive way. These patterns suggest that DCG overleveraged on GBTC, and with the discount widening, it has been difficult for the company to correct course. Ram Ahluwalia has captured it beautifully in this twitter thread, I recommend reading.

The drama is ongoing, Gemini, through its Earn product, and FTX have joined the fray, making this a multi-party affair. FTX has even taken legal action against Grayscale, presumably to extract as much money as possible from the bankruptcy proceedings.

I recognize that the various twists and turns of this saga may unnerve investors. Yet, the heart of this extensive narrative is to acquaint readers with the abundant drama and subplots encircling the trust. Despite all the commotion, the trust has persisted, with the sole consequence being its failure to eradicate the discount, partly due to DCG being saddled with a significant portion of GBTC.

Investment case

The rationale to invest in Grayscale Bitcoin Trust is actually very simple. Why bother with the hassle of storing Bitcoin in a secure cold storage or taking the risk of leaving it on unreliable exchanges that in some cases are not legally equipped to work as custodians when you can simply buy GBTC at a discounted price? By purchasing GBTC, you effectively own Bitcoin and can keep it safe with a trustworthy fiduciary custodian like Coinbase, making it a much easier and safer investment option.

The primary concern lies in becoming entangled in the DCG/Genesis debacle and witnessing a further decline in the discount or a lag in GBTC’s growth compared to the rise of Bitcoin. While it is not a matter to be taken lightly, there are various possible situations where an individual who purchases GBTC now could emerge ahead.

For instance, currently there’s no redemption program for GBTC shares. However, with regulatory approval, a redemption program could come into play in the future. And with that, market participants could take advantage of any opportunities created by the deviation between the price and the NAV through arbitrage.

On the same note, the SEC has been giving Grayscale a tough time with their proposal to convert to a Bitcoin spot ETF, they have already rejected over a dozen applications for a Bitcoin spot ETF, including Grayscale’s latest proposal in June. Grayscale didn’t take that rejection lying down, they immediately sued the agency.

In court, things just got interesting. One of the judges actually said there was no evidence that Grayscale’s argument was flawed and the SEC’s argumentation was questioned. The SEC claims that Grayscale didn’t provide the right market data to support their claim that a Bitcoin spot ETF could guard against manipulation. But a judge said that the SEC needed to clarify what data Grayscale needed to provide. So, we’ll have to wait and see how this all shakes out.

There are a few more possibilities to consider that could ultimately lead to the liquidation of the trust, and that’s not something that Grayscale wants to see happen, given that it represents a significant source of their revenue. But, there is a potential intermediate solution that’s been suggested by Michael Sonnenshein, the CEO of Grayscale. He’s proposed a tender offer that would allow shareholders to sell up to 20% of their GBTC shares back to the company at a set price. It’s not a perfect solution, but it could provide some relief for investors who are looking to get out of the trust, while also giving Grayscale some flexibility in managing their holdings.

All said, there is a myriad of risks surrounding the trust, but so far it has remained insulated from most of them. The main issue is that the trust is holding an asset and currently trading at a significant discount. However, the lack of clarity on how to align the trust’s price with the underlying asset shouldn’t discourage investors. In fact, it presents an opportunity to buy Bitcoin at a hefty discount of 35%. The main risk I see, right now is what seems to be a synchronized effort by US authorities to remove the on-ramps to Bitcoin, which might be revealing an anti-crypto stance from the White House. In that case, one would probably be better off by holding Bitcoin in a hardware wallet, and not pursuing this strategy. This is not financial advice.

This text expresses the views of the author as of the date indicated and such views are subject to change without notice. The author has no duty or obligation to update the information contained herein. Further, wherever there is the potential for profit there is also the possibility of loss. Additionally, the present article is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Some information and data contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. The author trusts that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.

Leave a comment