Photo credit: Sam valadi

The world is becoming increasingly faster, and so do markets. However, this seems to be getting a bit extreme. The market went from total euphoria in February to extreme depression in March, and now, at the beggining of April, it seems ready to come back with a vengeance.

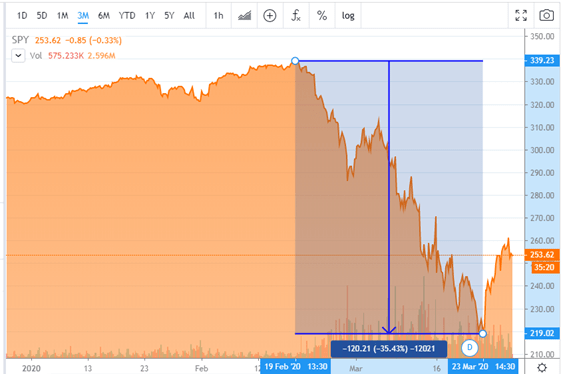

In February, the complacency ended in depression, with the market dropping 35% in one month.

(Source: Seeking Alpha)

(Source: Seeking Alpha)

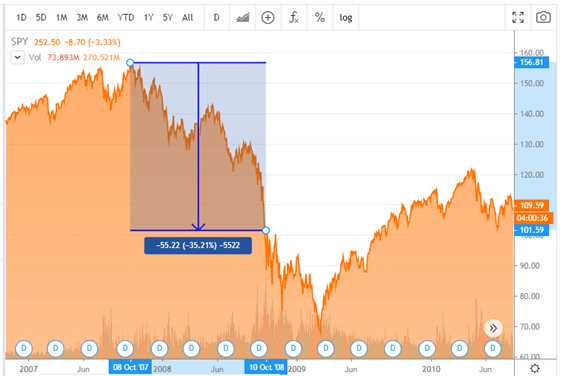

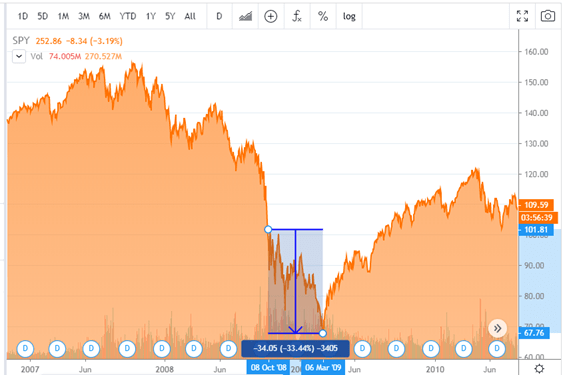

Just to offer some perspective, for you to have a market drop of the same magnitude during the great recession, you need almost a year. The final capitulation of the market took, with a movement similar in magnitude, five months.

(Source: Seeking Alpha)

(Source: Seeking Alpha)

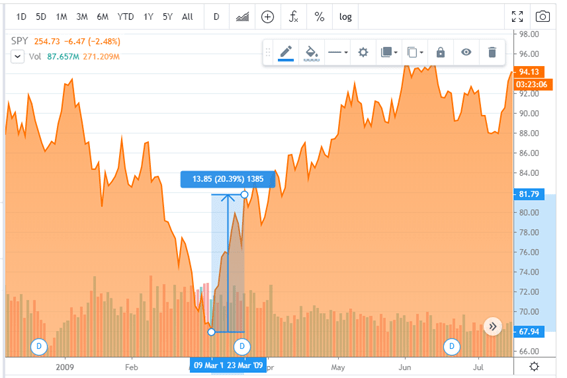

Even after the complete capitulation, it took the market 14 days to exit the bear market.

(Source: Seeking Alpha)

The 2000 dotcom meltdown took one and a half years to drop 35%.

(Source: Seeking Alpha)

That goes a long way to show that the present market moves are manic. The time frame for the drops was hugely reduced, and the recovery rally was also tremendously fast. Why is this happening?

Spoon-fed investors are completely dependent on the Fed put. That creates a huge level of complacency delaying corrections in the market. Additionally, the extreme levels of the current stimulus are awful for price discovery. Hence, you have these wild moves, and nobody can really tell where the market is. For that, you would need to have a good grasp of the hurdle rate of investment for the next couple of years. With so many misguided people thinking that we’ll have ZIRP forever, many market participants are valuing companies at close to infinity.

The passive investment vehicles are also responsible for that, especially on the way down. During panics, everyone is trying to get out of the door at the same time. ETFs make it worse. Investors are trying to liquidate what, in reality, are long positions in several equities, using just one door. When everyone is flocking to the exit, that door becomes too small. The result is that all securities are affected almost the same way without regard to the differences between them.

Algorithms are also responsible for the carnage. Yes, they’ve made trading much more efficient, most of the time. Except that, during panics, they amplify movements in a mesmerizing way. The algos are very sensitive to price action, meaning that in a very volatile environment, they tend to provoke wide swings.

The bottom-line is that all these instruments that have made really hard the life of the people searching for mispricing in the market, ironically, during panics tend to generate huge opportunities for them.

Getting back to our question, the renewed expansion of the Fed’s balance sheet is, clearly, inflationary in the long run. However, in the short term, there are several offsetting deflationary forces. Unemployment is likely to rise, and the same for bankruptcies. We are likely to be in a recessionary scenario for a while. Even with the massive monetary stimulus, operating profits will likely decline until 2021.

The likely outcome is that stocks won’t be immune to lower operating profits. If that’s the case, the current market move won’t be more than a bear market rally.

If you liked this post, why not subscribe? We won’t spam you.

Additional disclosure: This text expresses the views of the author as of the date indicated and such views are subject to change without notice. The author has no duty or obligation to update the information contained herein. Further, wherever there is the potential for profit there is also the possibility of loss. Additionally, the present article is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Some information and data contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. The author trusts that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.

Leave a comment