Summary

- The Fed’s move to placate the high-yield corporate bond market reinforced my conviction in the gold trade.

- Gold has performed very well. So well, that we are considering to take it to another level.

- We reviewed a set of gold producers to understand the most likely to benefit from the gold uptrend.

Original post: Seeking Alpha

Photo credit: James Mathews

At the beginning of January, I started to draft an article about my one-way bet for the year ahead. You know, that typical new year’s post that ends up completely wrong by the end of it. Basically, the idea was to bet against the high-yield corporate credit market. The COVID-19 events made me even more convict on that bet. However, it also increased my conviction on the gold trade.

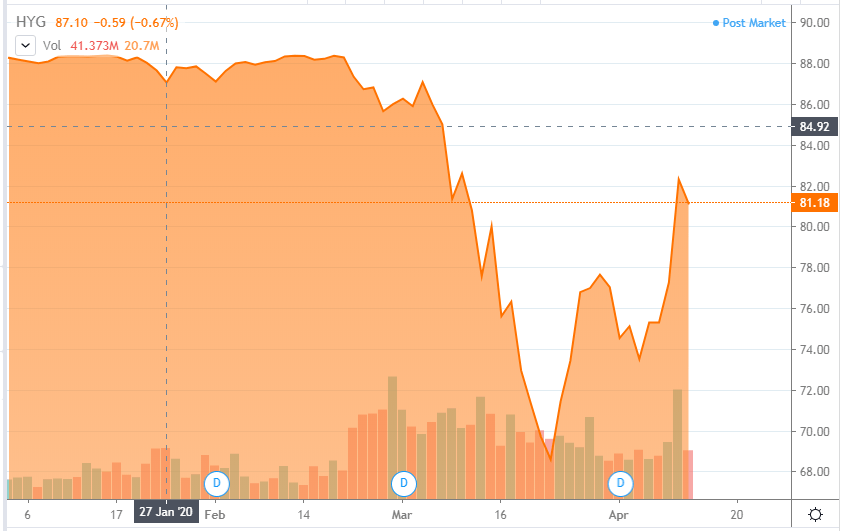

Actually, because I’m very conservative regarding short positions, I ended up devoting most of my attention to the gold trade and neglected the HY short. It was unfortunate since that trade would have worked wonders, at least, until the moment the Fed announced that it was buying HY bonds.

Source: Seeking Apha

It was unfortunate because had I shorted it when I thought, I would still be making money. Nevertheless, not all was lost because the Fed’s HY program was another step confirming my thesis on Gold. The Fed is determined to do whatever it takes to avoid problems in the credit market. I had advanced the idea that the Fed would go for high stake game in a previous missive:

Is it likely that the Fed goes to QE5? I think so. Chairman Powell comes from the private equity world, and he must be terrified with the prospect of having huge cracks opening in the corporate debt market. The BBB segment of the market has been a worry for a long time, and I believe that the Fed will go far in its efforts to keep the market together. Slashing the Fed Funds rate by 100 bps to 0.0-0.25% and launching a $700B liquidity program are steps in that direction.

That was even more accurate than I thought. Instead of months, they took only two weeks to rescue the high-yield market. More money printing, coupled with the same gold output, you do the math. I have made the case in favor of a simple strategy on the SPDR Gold Trust ETF (GLD), however now I want to explore miners. You may ask why.

Source: Seeking Apha

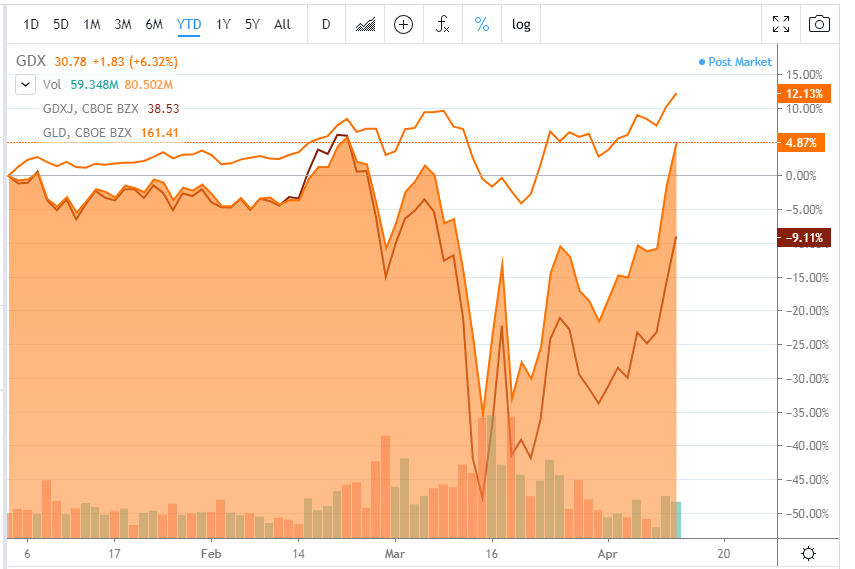

Well, so far, the GLD has overperformed both the VanEck Vectors Gold Miners ETF (GDX), and the VanEck Vectors Junior Gold Miners ETF (GDXJ), but, as you can see, both are recovering very fast from their prior lows.

There are two reasons why I think that miners now have the conditions to outperform. First, the commodity they produce is on the rise, having appreciated around 12%, year-to-date. Second, the Fed has just helped almost every company with debt with the two trillion USD program for High Yield corporate debt. And third, the current monetary and fiscal stimulus is reflationary for stocks in general.

Here, we have two main options. We can go with leveraged miners, with high-cost structures (or, mainly, in development/exploration phases), and hope this tide lifts all boats. That tends to be a very profitable exercise if done right. Or, we can choose established gold producers, just hoping to, quietly, follow the trend.

Getting a feel on gold producers

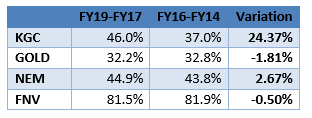

To get a feel on gold miners, I’ve collected some indicators on four companies: Barrick (GOLD), Newmont (NEM), Franco Nevada (FNV), and Kinross (KGC). These are, basically, the three biggest GDX holding, plus the biggest GDXJ holding. The idea is to have one junior miner to contrast with the majors.

While doing this analysis, I’ve dabbled through the financials trying to understand which indicators could provide the best picture. While doing this analysis, I’ve dabbled through the financials trying to understand which indicators could provide the best picture. Therefore, I’ve averaged the 3-year gross margin for two periods: FY19 to FY17, and FY16 to FY14.

Source: Seeking Alpha; Author’s Computations

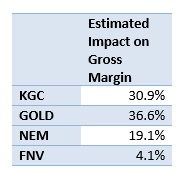

As we can see, Kinross stands out, having improved its gross margin significantly during the last few years. That makes sense because Kinross is a junior producer that has been making its way towards profitability. Now, these results excited my curiosity, and I turned my attention to the sensitivity of the gross margin to variations of the gold price. Therefore, I ran a couple of regressions, to try to measure the effect of a $400 variation of the price of gold in each company’s gross margins.

Source: Author’s Computations

Let’s take this result with a grain of salt. Although the statistics seem robust, these are just indicative results. Additionally, that was the result of a simple linear regression, bear in mind that for higher variations of the gold price, the impact on gross margin won’t be linear. Therefore, I’m just considering the magnitude of the results and not their absolute values. The results do seem to suggest that both Barrick and Kinross are the most sensitive to a variation of the gold price. I was expecting Kinross to be very sensitive, but I thought Barrick would be less sensitive.

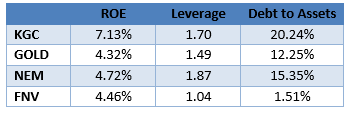

Now, turning to the return on equity, we’ve made an adjustment by using three-year average profits for this figure. The industry is highly volatile, and we wanted to harmonize it. Kinross almost doubles the major producers. However, Kinross is also the company with the highest debt-to-assets level which helps to explain the higher ROE. As a side note, the ROE is a good reflex of the poor performance of the companies in the gold sector.

Source: Author’s Computations based on figures from Seeking Alpha

Takeaways

The simplest way to play a gold price surge with miners is clearly by holding a diversified basket of gold producers. Both the VanEck Vectors Gold Miners ETF and the VanEck Vectors Junior Gold Miners ETF can do the trick.

If you are interested in searching for alpha, I think that Kinross might be an interesting move, since it is clearly the company more sensitive to the gold price (of all the reviewed). Barrick is also an interesting move since it is more sensitive to gold price than perceived by the market.

All-in-all, investors should be aware that returns for this industry have been poor, and a change in the outlook is very much dependent on the gold price trending higher. If that materializes, the gains have the potential to be sizable. Be as it may, investing in miners should be combined with a diversified portfolio. And, remember that in specific periods it worked well, but as a long term buy-and-hold, miners have performed poorly.

Source: Seeking Alpha

Disclosure: I am/we are long GLD, KGC, GOLD. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: This text expresses the views of the author as of the date indicated and such views are subject to change without notice. The author has no duty or obligation to update the information contained herein. Further, wherever there is the potential for profit there is also the possibility of loss. Additionally, the present article is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Some information and data contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. The author trusts that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.

Leave a comment