One can make the argument that the best thing emanating from the Randgold takeover by Barrick (GOLD) was the CEO. As the merger negotiations finalized, Mark Bristow became the new Barrick CEO. Mr. Bristow has a remarkable track record as Randgold’s CEO.

Picture credit: Mines and Money

He credits much of Randgold’s success to the discipline of investing only in tier one assets (at least 10 years of asset life, annual production of 500,000 ounces, and 15% IRR at 1,200 USD gold price), and not following unconstrained expansion when the gold price is rising. Now, he wants to do the same at a bigger scale at Barrick.

(Source: Investing.com)

Now, look at Randgold’s performance since 1998. If the rule is that mining is a terrible business, then Randgold was the golden exception, striking close to 1000% gains since 1998. Given that Barrick has some of the top mines in the industry, we can only expect that Mark Bristow replicates the same recipe.

The strategy is simple, you have to focus on the quality of the asset, and never run after a gold price surge. Therefore, Barrick has gone through an asset disposal program to sell assets that don’t fit the tier 1 criteria. Additionally, the company has reduced its debt significantly. Since 2013 the company reduced debt from $13.4 billion to $1.9 billion. Now, that can’t just be attributed to Bristow, he just landed on Barrick in 2019, but it is a testament to the strategy of the board following the bust in the gold price in 2013.

Source: Barrick Investor Q1 presentation

This structure, based on low debt, and high-quality assets, will allow Barrick to better cope with the cyclicality of the industry. Namely, it will likely do very well during high gold price periods. In the down years, it will have cash reserves to pursue consolidation in the industry. If done well, it will replicate the virtuous cycle enjoyed by Randgold, during its life as an independent producer.

Likely, we’ll see Barrick taking advantage of the current gold price to accumulate cash, and, on the lower part of the cycle, I expect to see Barrick cherry-picking companies for industry consolidation. If done from a vantage standpoint, shareholders will reap the rewards from being disciplined in a cyclical industry.

Investor takeaways

I expect the company to deliver on this strategy. The current background is favorable to gold prices. Low-interest rates coupled with monetary largesse have, historically, been supportive of bullion prices. Therefore, I anticipate that they deliver accordingly. I expect to see a good generation of cash-flow and debt reduction, without rushed M&A nonsense on the gold sector.

I expect the company to deliver on this strategy. The current background is favorable to gold prices. Low-interest rates coupled with monetary largesse have, historically, been supportive of bullion prices. Therefore, I anticipate that they deliver accordingly. I expect to see a good generation of cash-flow and debt reduction, without rushed M&A nonsense on the gold sector.

Summing-up, I’ll be testing the following hypothesis:

H0: Barrick will improve its cash-flow generation during the uptrend in gold prices, reducing its debt and, possibly, improving dividends.

H1: There won’t be any stretched M&A of other gold producers (or gold assets) during the bull market in gold.

If any of these hypotheses proves false, the thesis in this text becomes seriously impaired and will have to be revised.

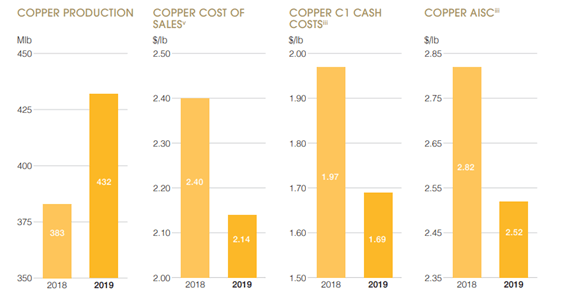

Bonus track: Copper

To clarify, I’m long Barrick, because I see it as a good gold play. For my purposes, I’ll need the gold price to go up. If I conclude that the gold price won’t go up, I will likely cash-out. Gold miners are a terrible business, and, for investors to make decent returns, the acquisition price plays a huge role. The current price makes sense to me if the gold price keeps going higher and reaches a higher plateau than the current level. If that’s the case, a buy-and-hold strategy might make sense if the company delivers on its strategy, and we have a type of Randgold 2.0.

However, for that to happen, the company will have to change its posture from being in the gold business to be in the mining business. That means embracing new trends in the industry. One of them relates to improving the copper extraction from gold orebodies. New methods seem to add synergies to the extraction of other metals present in the gold orebody. Therefore, it shouldn’t come as a surprise that Mark Bristow announced that Barrick would focus more on recovering copper.

More recently, he even admitted that they might be interested in copper miners. Does it make sense? It might. A few paragraphs ago, I stated that this is not the time for M&A action in the gold sector, but what about the copper sector?

(Source: Finviz)

Well, copper is now trading around 28% below its 2018 high. During the last two years, copper has been on a downtrend, likely the companies in the sector are hurt, and opportunities for consolidation are, probably, more attractive than in gold.

This is an interesting development, and it will certainly change the industry going forward. For my investment horizon, it might not be too meaningful, but in a buy-and-hold perspective, this adds an extra dimension of risk (and reward).

Therefore, If I were to stay for the long term, I would add an extra hypothesis:

H2: Barrick will increase its copper production and it will do so profitably.

(Source: Barrick report)

So far, so good, but I would keep an eye on it.

Disclosure: I am/we are long GLD, KGC, GOLD. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: This text expresses the views of the author as of the date indicated and such views are subject to change without notice. The author has no duty or obligation to update the information contained herein. Further, wherever there is the potential for profit there is also the possibility of loss. Additionally, the present article is being made available for educational purposes only and should not be used for any other purpose. The information contained herein does not constitute and should not be construed as an offering of advisory services or an offer to sell or solicitation to buy any securities or related financial instruments in any jurisdiction. Some information and data contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. The author trusts that the sources from which such information has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based.

Leave a comment